“The 2026 Wealth-Builder Series” is designed to follow your comprehensive guide by diving deeper into specific, actionable pillars of financial independence.

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

In Part One of our wealth-builder series. SAVE MONEY FUND YOUR FUTURE: A COMPLETE GUIDE TO HIGH-YIELD SAVINGS ACCOUNTS AND INVESTMENT STRATEGIES FOR BUILDING WEALTH IN 2026.

We discussed the importance of high-yield savings accounts (HYSAs). But in 2026, simply having “some money set aside” isn’t enough.

Series Part 2: The Tiered Emergency Fund: Protecting Your Progress in a Volatile 2026.

With the economic shifts we’ve seen over the last three years, the “3-6 months of expenses” rule has evolved into the Tiered Emergency Fund.

Why the Old Rules Changed

In 2023, high inflation made cash feel like it was losing value. In 2026, with inflation stabilized at 2.5% but job markets becoming more specialized, your safety net needs to be more strategic. A tiered approach ensures your money is protected but still earns a competitive return.

How to Structure Your Tiers

Instead of keeping $20,000 in a single account, split your safety net into three distinct “buckets”:

- Tier 1: Immediate Liquidity (The “Right Now” Fund)

- Amount: $1,000 to one month of expenses.

- Location: A standard savings account linked to your checking.

- Purpose: Instant access for car repairs or medical co-pays.

- Tier 2: The High-Yield Core (The “Safety” Fund)

- Amount: 3 months of expenses.

- Location: High-Yield Savings Account (HYSA) earning 3.8%–4.2% APY.

- Purpose: Job loss or major home repairs.

- Tier 3: The Growth Buffer (The “Extended” Fund)

- Amount: 3+ months of expenses.

- Location: A 6-month CD ladder or a Money Market Account.

- Purpose: Long-term protection that earns a slightly higher rate than Tier 2.

The 2026 Refill Strategy

If you dip into Tier 1, your automation should temporarily pivot. Redirect your $100 monthly “wealth-building” transfer back into Tier 1 until it’s topped off, then resume your long-term investment strategy. This keeps your foundation solid without halting your momentum entirely.

Series Part 3: From Saver to Investor: Navigating Index Funds and ETFs in 2026

You’ve mastered the high-yield savings account and the CD ladder. Now, it’s time to move up the “Wealth Ladder.” To truly build wealth in 2026, you must transition a portion of your automated savings into the stock market through low-cost Index Funds and ETFs.

The Power of the “Set and Forget” Portfolio

In 2026, robo-advisors have made it easier than ever to access diversified portfolios. While your HYSA protects you, the stock market grows your purchasing power.

2026 Diversification Model:

- Total Stock Market ETF: Provides exposure to thousands of companies.

- International Growth Fund: Taps into emerging markets that have stabilized since 2024.

- Dividend Aristocrats: Funds that pay you cash just for owning them—perfect for reinvesting.

Dollar-Cost Averaging (DCA) is Still King

The secret isn’t timing the market; it’s time in the market. By automating a $100 or $200 monthly transfer into a robo-advisor or brokerage account, you buy more shares when prices are low and fewer when they are high.

| Investment Type | Risk Level | Expected Return (Long Term) |

|---|---|---|

| High-Yield Savings | Low | 3.5% – 4.2% |

| S&P 500 Index Fund | Moderate | 7% – 10% |

| Focused Tech ETF | High | 10% + |

When to Make the Jump

Once your Tier 2 emergency fund (from Part 2 of this series) is full, every “extra” dollar should be split: 50% toward your high-yield savings for short-term goals and 50% toward your investment portfolio for 2030 and beyond.

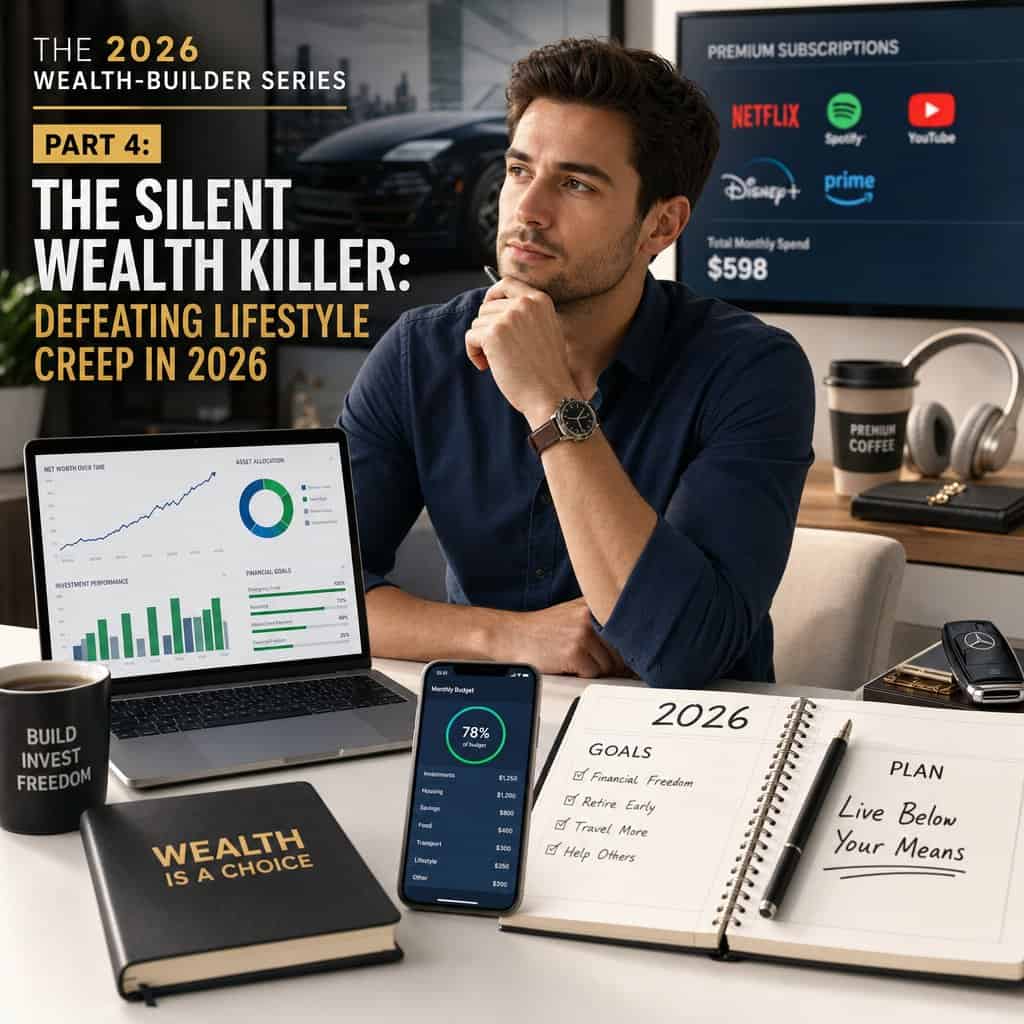

Series Part 4: The Silent Wealth Killer: Defeating Lifestyle Creep in 2026

You’ve set up the accounts, automated the transfers, and started investing. But there is one final hurdle that stops most people from reaching financial independence: Lifestyle Creep.

What is Lifestyle Creep?

As your income grows in 2026—perhaps through a promotion or a side hustle—your spending naturally tends to rise to meet it. That $500 raise often disappears into a more expensive car lease or premium subscriptions before it ever hits your high-yield savings.

The “50% Raise Rule”

To build wealth in 2026, adopt the 50% Raise Rule. Whenever you get an increase in income:

- 50% goes to your “Future Self”: Immediately increase your automated transfers to your HYSA or Investment account.

- 50% goes to your “Present Self”: Enjoy the fruits of your labor by increasing your lifestyle or fun budget.

This allows you to enjoy your success while ensuring your “Wealth-Builder” engine accelerates.

Audit Your Digital Leaks

In 2026, the average consumer has 12+ digital subscriptions. Use the tools mentioned in our first article—robo-advisors and digital finance apps—to track your “burn rate.”

- Action Step: Every three months, do a “Subscription Slash.” If you haven’t used a service in 30 days, cancel it and redirect that exact monthly amount into your Tiered Emergency Fund.

Staying the Course

Wealth isn’t built in a day; it’s built in the habits you repeat every month. By combining high-yield accounts, smart diversification, and a shield against lifestyle creep, you aren’t just saving money—you are funding a future where work is optional.

Series Part 5: Master mindset shifts for financial success, defeat lifestyle creep, apply the 50% Raise Rule, and audit digital leaks with the 2026 Wealth-Builder series to fund your future.

Why Logic Isn’t Enough to Build Wealth

By now, you have likely established the technical foundations of your financial house. You have explored high-yield savings accounts, understood the mechanics of CD ladders, and perhaps even initiated automated transfers to a robo-advisor. However, as we progress through the 2026 Wealth-Builder Series, we must address the most significant variable in the wealth equation: you.

In 2026, the barrier to building wealth is rarely a lack of information. Instead, it is the psychological friction of living in a hyper-consumptive society. Building wealth is 20% head knowledge and 80% behavior.

Even the most sophisticated investment strategy will fail if it is undermined by impulsive spending or a lack of emotional discipline. This article serves as your guide to mastering the “inner game” of finance, ensuring that the money you save actually stays saved.

Understanding the Silent Wealth Killer: Lifestyle Creep

The “50% Raise Rule”: A Framework for Sustainable Growth

Auditing Your Digital Leaks: The 2026 Subscription Crisis

The Behavioral Psychology of “Naming” Your Money

The Emotional Intelligence (EQ) of Wealth: Why EQ Beats IQ

Practical Implementation: Your 2026 Wealth-Builder Checklist

Conclusion: Funding a Future Where Work is Optional

If you are ready to take the next step in your financial journey, explore our other articles in the series or create visual trackers for your savings goals.

Series Part 4: The Silent Wealth Killer: Defeating Lifestyle Creep in 2026

SERIES PART 5. MASTER MINDSET SHIFTS FOR FINANCIAL SUCCESS, DEFEAT LIFESTYLE CREEP, APPLY THE 50% RAISE RULE, AND AUDIT DIGITAL LEAKS WITH THE 2026 WEAL

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We don’t offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized advice. Track your progress for a better credit journey.

Written content – “Please view our full AI Use Disclosure.

“We improve our products and advertising by using Microsoft Clarity to see how you use our website. By using our site, you agree that we and Microsoft can collect and use this data. Our privacy policy has more details.”