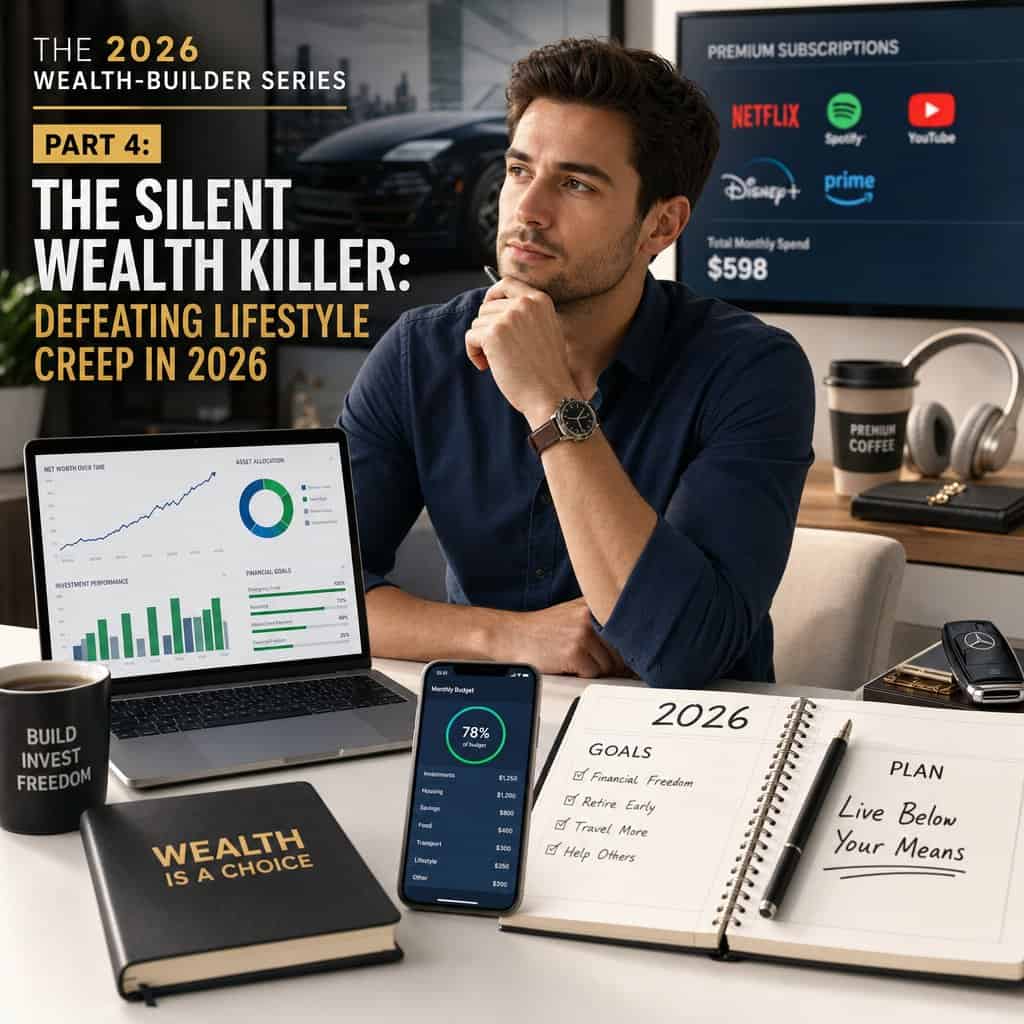

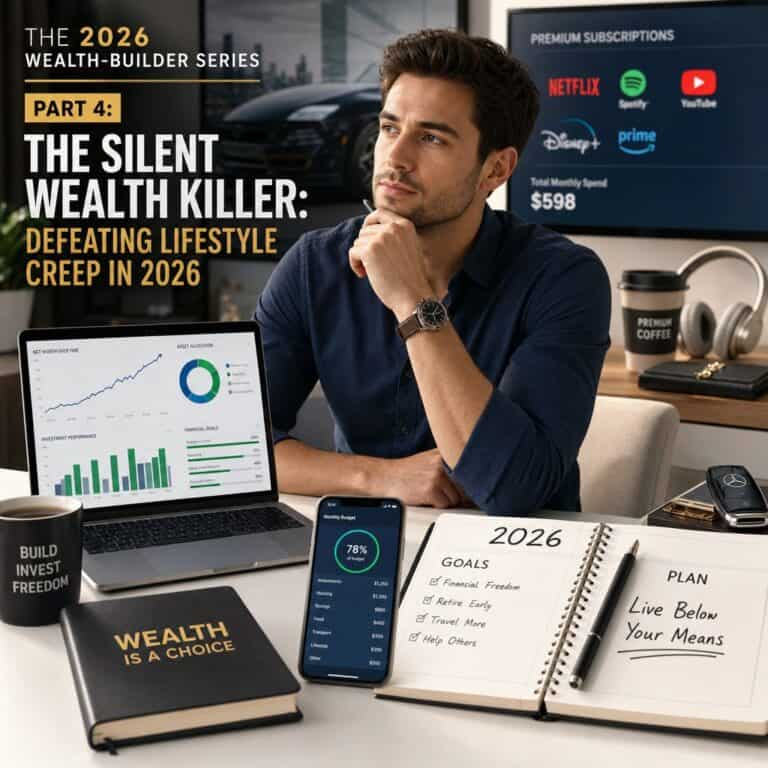

Lifestyle Creep: Defeating the Silent Wealth Killer in 2026.

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

DON’T HAVE TIME TO READ THE FULL ARTICLE. HERE’S WHAT YOU ARE MISSING.

You worked hard for that promotion or new job. Suddenly, more money lands in your account each month.

But here’s what most people never mention: within six months, that extra income seems to disappear into nicer dinners, a better apartment, or a handful of subscriptions you barely remember signing up for.

This is lifestyle creep. It’s why even six-figure earners can still live paycheck to paycheck.

Lifestyle creep sneaks in when spending rises to match your income. You end up with no extra wealth, even though you’re making more money.

The good news? You can enjoy your success and build wealth at the same time. You don’t have to pick between living well today and securing your future.

In this guide, you’ll find practical strategies to halt lifestyle creep before it drains your paycheck. The 50% Raise Rule helps you split income boosts between living well now and funding your future.

You’ll also learn how to spot and fix digital spending leaks that quietly siphon off hundreds every month.

Key Takeaways

- Use the 50% Raise Rule to split income increases between current enjoyment and future wealth building

- Review and cancel unused subscriptions every three months to redirect wasted money into savings

- Build automatic habits that grow your wealth without requiring constant willpower or sacrifice

Understanding the Mechanics of Lifestyle Creep

Lifestyle creep shows up as small, almost invisible spending increases. Over time, these add up and eat away at your wealth-building potential.

You probably won’t notice these changes until they’ve already cost you thousands.

How Small Spending Increases Steal Your Wealth

Lifestyle creep is basically a math problem. If you earn $50,000 and get a $5,000 raise, your new salary becomes $55,000.

Increase your spending by just $400 a month and you’ve burned through $4,800 of that raise each year.

That $400 might look like this:

- $15 more on coffee and lunch each week

- One extra streaming service at $20 a month

- Upgrading your car payment by $100 monthly

- Eating out twice more per month at $50 each time

These changes feel reasonable. You worked for that raise, right?

But here’s what you’re actually giving up: $4,800 invested every year at 8% returns becomes $27,500 in a decade. In 20 years, it could be $100,000.

The real loss isn’t just today’s spending. It’s the compound growth you’ll never see.

Common Triggers for Cost of Living Escalation

Income bumps trigger the most lifestyle creep. Promotions, raises, bonuses, and new jobs all tempt you to spend more.

Your brain tells you that higher earnings justify higher expenses. Social comparison kicks in, too.

When friends upgrade their homes or cars, you feel pressure to keep up. Social media amplifies this, showing you endless upgrades and purchases.

Major life events can also push spending up. Getting married, having kids, or moving to a new city often brings permanent cost increases that go beyond what’s really needed.

Frequent lifestyle creep triggers:

- Annual salary increases

- Job promotions

- Tax refunds

- Work bonuses

- Peer group changes

- Moving to higher-cost areas

Why It’s More Dangerous in 2026

The 2026 economy makes lifestyle creep tougher to spot. Digital payment systems hide your real spending.

When you tap your phone or click to buy, purchases don’t feel as real as handing over cash.

Subscription services have exploded—up 40% since 2020. Now, the average person juggles 12 to 15 recurring charges.

Each one might seem tiny at $10 or $20 a month, but together they can quietly pull $200 or more from your account every month.

Buy-now-pay-later services are everywhere. They split purchases into installments, so a $200 item feels like a $50 splurge.

Your brain barely notices the full price. Inflation in 2026 also blurs the picture.

When prices rise 3% to 4% a year, it’s easy to think your spending is just keeping up. But often, you’re upgrading quality at the same time, doubling the hit to your budget.

The 50% Raise Rule: Balancing Growth and Enjoyment

When your income goes up, you need to give that money a job before it lands in your checking account. Split every raise down the middle: half for future wealth, half for living better now.

Setting Automated Transfers for Your Future Self

The first 50% of any raise goes straight to your future self. Set up automation within 24 hours of your first bigger paycheck.

Figure out how much extra you’re getting each month. If your salary jumps from $50,000 to $55,000, that’s $5,000 more a year—about $417 monthly. Half is $208.

Hop into your bank’s transfer settings and create a new automatic transfer for $208. Schedule it to move from checking to your high-yield savings or investment account the day after each paycheck arrives.

This happens before you really see the money. Before you even have a chance to think about it.

Studies show automation boosts long-term savings rates by over 40%. The money moves without you needing to rely on willpower.

Your savings rate should climb with every raise. If you saved 15% of $50,000, you should be closer to 18-20% of $55,000 now.

Adjusting Your Lifestyle Budget Responsibly

The other 50% is for enjoying your success. Don’t treat it as guilt money or leftovers—use it with intention.

Pick three upgrades that actually matter to you. Maybe better groceries, a nicer gym, or more reliable transportation.

Maybe you dine out twice a month instead of once. Watch out for the subscription trap.

Adding Netflix, Spotify, meal kits, and workout apps seems harmless but adds up fast. In 2026, the average person has 12+ digital subscriptions.

Try to replace old services instead of just stacking new ones. Use your $209 a month on what matters—if you spend $100 on groceries and $50 on the gym, bank the extra $59 or throw it at debt.

Small upgrades that always match your raises block wealth building. Intentional choices let you enjoy life and make progress financially.

Activating Your Wealth-Builder Engine

The 50% Raise Rule turns income growth into real wealth. You feel a lifestyle boost right away, but your net worth climbs in the background.

Check your progress every quarter. Open your savings or investment dashboard and compare your balance to three months ago.

You should see the increase. Someone who saves half their raises builds 4-7x more wealth over a career than someone who saves none—even if their income is the same.

Compound growth works on the money you actually save, not what you intended to save. Each raise you split this way makes work a bit more optional and financial stress a bit lighter.

Auditing and Slashing Your Digital Spending

Most Americans waste $273 a month on forgotten subscriptions. To plug these “digital leaks,” you just need a simple system: track what you pay for, cut what you don’t use, and send those savings straight to your emergency fund.

Tracking Subscriptions with Finance Apps

Your bank statement hides the truth about your spending. Apps like Rocket Money, Truebill, or Mint can scan your accounts and list every recurring charge in one spot.

Link your checking account and credit cards to one of these apps. Within a day, you’ll see a full list of monthly subscriptions.

The apps group each charge and show you the total leaving your account each month. Set up spending alerts for new subscriptions.

Most people sign up for free trials and forget to cancel. An alert gives you a 48-hour heads-up to decide if you want to keep the service.

Check your subscription list weekly for the first month. You’ll probably spot charges you don’t recognize—old streaming services, one-time app downloads, or memberships you meant to cancel ages ago.

Executing Your Quarterly Subscription Slash

Mark your calendar for four dates in 2026: March 19, June 19, September 19, and December 19. These are your Subscription Slash days.

If you missed this month, start with the next quarterly calendar month and track four consecutive quarters, or for one calendar year.

On each date, open your finance app and review every subscription. Ask yourself, “Did I use this in the last 30 days?”

If the answer’s no, cancel it right then and there.

Common subscriptions to review:

- Streaming services (Netflix, Hulu, Disney+, HBO Max)

- Music platforms (Spotify, Apple Music, YouTube Premium)

- Fitness apps and gym memberships

- Cloud storage

- Gaming subscriptions

- News and magazine apps

- Meal kit deliveries

- Software tools

Write down the dollar amount for each canceled subscription. Add up these amounts to see your total monthly savings.

Redirecting Savings to Tiered Emergency Funds

As soon as you cancel a subscription, open your bank’s app or website. Set up an automatic monthly transfer for the same amount you just freed up.

If you canceled a $14.99 streaming service, set a $14.99 monthly transfer to your high-yield savings account. Schedule it for the day your paycheck lands, so you barely notice it’s gone.

If you don’t redirect that money, it just disappears into other spending. Your brain probably won’t notice $15 missing from checking, but your emergency fund will thank you for the extra $180 a year from one canceled subscription.

Stack these redirected amounts each quarter. Cancel $50 worth in March, $30 in June, and $25 in September? That’s $105 a month heading into savings—$1,260 a year toward your Tier 1 or Tier 2 emergency fund.

Building Habits That Outsmart Lifestyle Inflation

The real difference between people who build wealth and those who just earn more comes down to habits. Monthly routines and channeling income increases into the right accounts help your money work harder than lifestyle temptations can pull.

Monthly Wealth-Building Routines

Set a recurring reminder for the first of every month for your financial review. Give yourself 15 minutes to check account balances, review last month’s spending, and confirm your automated transfers went through.

Track three key numbers: total savings rate, investment contributions, and discretionary spending. Jot them down in a notebook or spreadsheet.

Over time, patterns emerge—sometimes not the ones you want. You’ll spot if lifestyle inflation is quietly eating away at your progress.

Every quarter, do your Subscription Slash. Open your banking app and review all recurring charges from the last 90 days.

Cancel anything you haven’t used in a month. The average person wastes $50–$200 monthly on forgotten subscriptions—kind of wild when you think about it.

Redirect every dollar you cut. Cancel a $15 streaming service? Bump up your HYSA transfer by $15 that same day. That’s how you turn found money into actual wealth, not just extra spending.

Leveraging High-Yield Accounts and Diversification

Apply the 50% Raise Rule to every income increase in 2026. When you get a raise, bonus, or side income boost, split it in half before you let lifestyle creep in.

Put the first 50% on autopilot into wealth-building accounts. Boost your HYSA, increase investment deposits, or add to your emergency fund. Set up the transfer right away—don’t wait until next week.

Spend the other 50% on intentional lifestyle upgrades. That way, you actually enjoy your success instead of feeling deprived. Want to take a better vacation or eat out more? Use this half for that.

Bank of America Institute shows about 20% of households earning over $150,000 still live paycheck to paycheck. Most of that happens because income bumps go straight to lifestyle upgrades, not wealth building.

Your HYSA keeps your emergency fund liquid and earning. Diversified investments give you long-term growth. Together, they form a foundation that prevents lifestyle creep from sneaking up on your financial progress.

Psychological Traps and Social Pressures

Your brain can work against you when you’re trying to build wealth. Friends and social algorithms constantly show you a life you think you should have.

Social media creates nonstop pressure to spend. Your own mind convinces you every upgrade is somehow necessary.

Keeping Up with Peers in the Digital Age

Instagram and TikTok bombard you with curated highlights 24/7. You see new cars, fancy vacations, and shopping hauls—but never the credit card statements or financial anxiety behind them.

This leads to “comparison spending.” You buy things not because you need them, but because everyone else seems to have them.

In fact, a 2026 study shows people who spend more than two hours a day on social media drop 30% more on discretionary stuff than those who don’t.

The dopamine rush from likes and shares fuels this, too. Post a new purchase, get positive feedback, and your brain lights up. Suddenly, you’re buying partly for the social validation, not just the thing itself.

Your peer group matters more than you think. If your friends eat at pricey restaurants or take big trips, you’ll feel pressure to join in—or risk feeling left out.

Redefining Success and Contentment

Success in 2026 and beyond often means visible purchases, not invisible wealth. A fat investment account won’t earn you Instagram likes, but a shiny new watch might.

Try to separate looking wealthy from being wealthy. Someone with a $70,000 car might have $200,000 in debt, while the person with a 10-year-old Honda could have half a million invested.

- Net worth growth year over year

- Months of expenses saved in emergency funds

- Percentage of income automatically invested

- Debt-to-income ratio dropping

Contentment comes from progress toward your goals, not from matching what others post online.

Celebrate your own financial wins, even if nobody else sees them. Max out your retirement account or pay off a debt—those are the real milestones.

Let your definition of success focus on freedom and security. Ask yourself if a purchase moves you closer to working because you want to, not because you have to.

Action Steps for Lasting Financial Success

Building wealth isn’t about a one-time sprint. You need a system you’ll actually stick with, month after month.

The two actions below help you keep momentum and adapt to life’s curveballs without wrecking your progress.

Review and Refine Your Financial Plan

Set a calendar reminder for the first Sunday of every quarter. Take 30 minutes to review your financial numbers from the past three months.

Check these four areas:

- Emergency fund balance: Compare it to your current monthly expenses.

- Subscription costs: Total up all recurring charges.

- Investment contributions: Make sure automated transfers went through.

- Income changes: Note any raises, bonuses, or side income.

Use a simple spreadsheet or finance app to track these numbers. Write down one specific change you’ll make based on what you find.

If your emergency fund hit your target, redirect those contributions to investments. If subscriptions crept up by $50, cancel services you skipped last month.

This quarterly check doesn’t take long—less time than a TV show. But it keeps your Wealth-Builder engine running and catches problems before they get out of hand.

Future-Proofing Against Evolving Temptations

Your income will probably grow over the next few years. Every raise or promotion brings new spending temptations you might not have even considered before.

Apply the 50% Raise Rule as soon as your income increases. Set up an automated transfer to your HYSA or investment account the same day you get confirmation of a raise.

Don’t wait until next month—just get it done and move on.

Watch out for these common wealth drains in 2026:

| Temptation | Alternative Action |

|---|---|

| Upgraded car lease | Keep current vehicle, invest the difference |

| Premium streaming tiers | Rotate services monthly, save $30-60 |

| Daily food delivery | Limit to weekends only |

Your past self made choices based on a lower income. Now, your future self needs you to lock in those wealth-building habits before lifestyle creep nudges your expectations higher.

If you are ready to take the next step in your financial journey, explore our other articles in the series or create visual trackers for your savings goals.

Series Part 4: The Silent Wealth Killer: Defeating Lifestyle Creep in 2026

SERIES PART 5. MASTER MINDSET SHIFTS FOR FINANCIAL SUCCESS, DEFEAT LIFESTYLE CREEP, APPLY THE 50% RAISE RULE, AND AUDIT DIGITAL LEAKS WITH THE 2026 WEAL

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We don’t offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized advice. Track your progress for a better credit journey.

Written content – “Please view our full AI Use Disclosure.

“We improve our products and advertising by using Microsoft Clarity to see how you use our website. By using our site, you agree that we and Microsoft can collect and use this data. Our privacy policy has more details.”