Series Part 5. Master mindset shifts for financial success, defeat lifestyle creep, apply the 50% Raise Rule, and audit digital leaks with the 2026 Wealth-Builder series to fund your future.

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

DON’T HAVE TIME TO READ THE FULL ARTICLE. HERE’S WHAT YOU ARE MISSING.

- Series Part 5. Master mindset shifts for financial success, defeat lifestyle creep, apply the 50% Raise Rule, and audit digital leaks with the 2026 Wealth-Builder series to fund your future.

- Why Logic Isn’t Enough to Build Wealth

- Understanding the Silent Wealth Killer: Lifestyle Creep

- The “50% Raise Rule”: A Framework for Sustainable Growth

- Auditing Your Digital Leaks: The 2026 Subscription Crisis

- The Behavioral Psychology of “Naming” Your Money

- The Emotional Intelligence (EQ) of Wealth: Why EQ Beats IQ

- Practical Implementation: Your 2026 Wealth-Builder Checklist

- Funding a Future Where Work is Optional

- Frequently Asked Questions (FAQs)

Why Logic Isn’t Enough to Build Wealth

By now, you have likely established the technical foundations of your financial house. You have explored high-yield savings accounts, understood the mechanics of CD ladders, and perhaps even initiated automated transfers to a robo-advisor.

However, as we progress through the 2026 Wealth-Builder Series, we must address the most significant variable in the wealth equation: you.

In 2026, the barrier to building wealth is rarely a lack of information. Instead, it is the psychological friction of living in a hyper-consumptive society. Building wealth is 20% head knowledge and 80% behavior.

Even the most sophisticated investment strategy will fail if it is undermined by impulsive spending or a lack of emotional discipline. This article serves as your guide to mastering the “inner game” of finance, ensuring that the money you save actually stays saved.

Understanding the Silent Wealth Killer: Lifestyle Creep

You’ve set up the accounts, automated the transfers, and started investing. But there is one final hurdle that stops most people from reaching financial independence: Lifestyle Creep.

What is Lifestyle Creep?

As your income grows in 2026—perhaps through a promotion, a successful side hustle, or a cost-of-living adjustment—your spending naturally tends to rise to meet it. This phenomenon is also known as “lifestyle inflation.” It is the reason why someone earning $200,000 a year can still feel like they are living paycheck to paycheck.

That $500 raise often disappears into a more expensive car lease, a larger apartment, or premium AI-driven subscriptions before it ever hits your high-yield savings. Lifestyle creep is dangerous because it is subtle. It doesn’t happen all at once; it happens one “small upgrade” at a time until your overhead is so high that you have no margin for error.

The Hedonic Treadmill: Why More Doesn’t Always Feel Like More

Psychologists refer to this as the “Hedonic Treadmill.” As you acquire more possessions or higher-status services, your expectations and desires rise in tandem. The “new car smell” eventually fades, and the luxury vehicle simply becomes the way you get to work. To stay on the path of the 2026 Wealth-Builder Series, you must recognize that your brain is wired to seek the next dopamine hit of a purchase, rather than the long-term peace of a growing net worth.

The “50% Raise Rule”: A Framework for Sustainable Growth

To build wealth in 2026, you need a system that allows you to enjoy your life today while protecting your future. Total deprivation is not a sustainable strategy; it leads to “frugal fatigue” and eventual binge-spending. Instead, adopt the 50% Raise Rule.

Whenever you get an increase in income, whether it is a bonus, a raise, or a tax refund, split that new money down the middle:

1. 50% Goes to Your “Future Self”

Immediately increase your automated transfers to your High-Yield Savings Account (HYSA) or your investment portfolio. If your paycheck increases by $400 a month, $200 of that should be diverted before you ever see it in your checking account. This ensures that your “Wealth-Builder” engine accelerates every time you succeed professionally.

2. 50% Goes to Your “Present Self”

The remaining 50% is yours to spend. Use it to upgrade your lifestyle, enjoy a higher-quality gym membership, or increase your travel budget. By allowing yourself to enjoy half of your success, you remove the psychological resentment that often comes with strict budgeting. This balance is what makes the 2026 Wealth-Builder Series a lifestyle rather than a temporary challenge.

Auditing Your Digital Leaks: The 2026 Subscription Crisis

In 2026, the average consumer has 12+ digital subscriptions. Between streaming services, AI productivity tools, premium news sites, and delivery memberships, “subscription fatigue” has become a major drain on personal wealth. These are “digital leaks”—small, recurring payments that seem insignificant individually but collectively sabotage your ability to save.

How to Conduct a “Subscription Slash”

Use the tools mentioned in our previous articles—robo-advisors and digital finance apps—to track your “burn rate.”

- The Action Step: Every three months, perform a “Subscription Slash.” Look through your credit card statements for any recurring charge. If you haven’t used a service in the last 30 days, cancel it immediately.

- The Redirection: Don’t just cancel the service; redirect that exact monthly amount into your Tiered Emergency Fund. If you cancel a $20/month streaming service, increase your automated savings transfer by $20. This turns a “leak” into a “link” to your financial freedom.

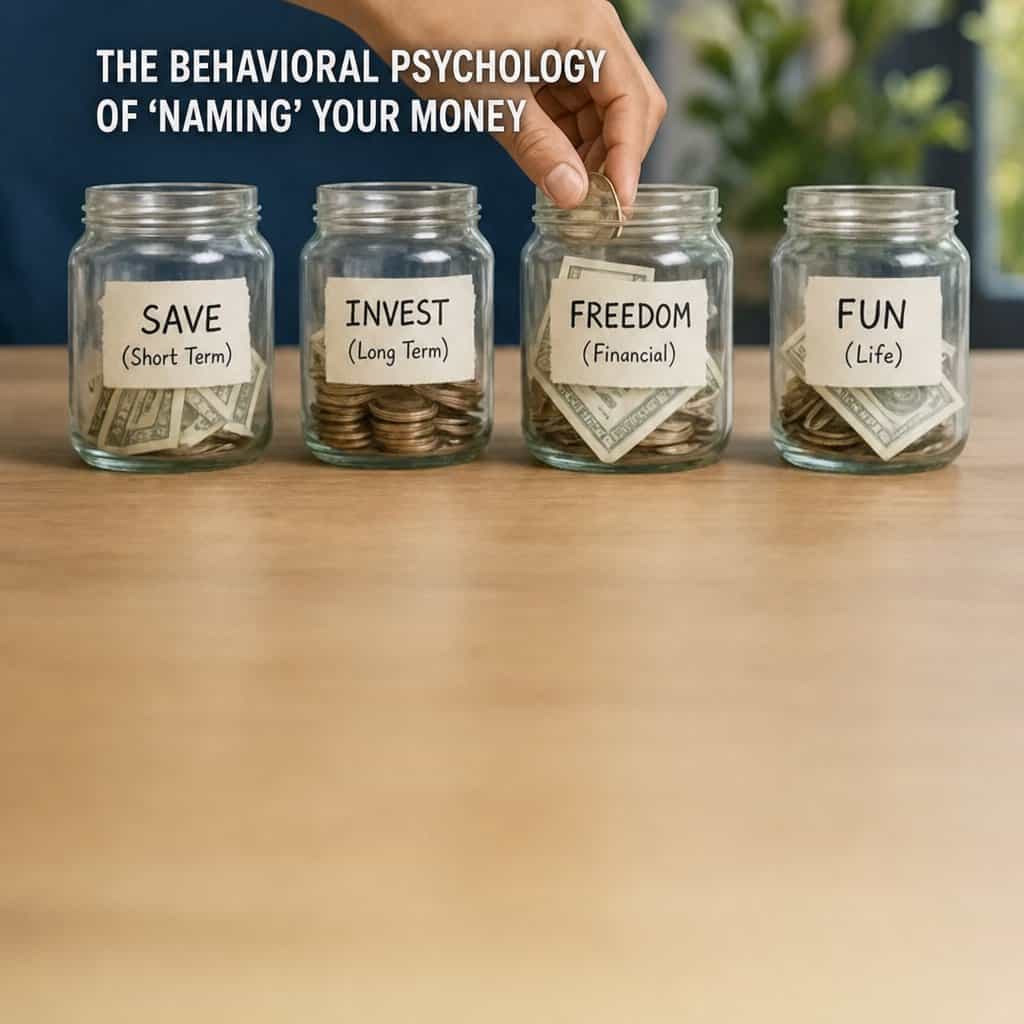

The Behavioral Psychology of “Naming” Your Money

One of the most effective psychological hacks for saving is the concept of “Mental Accounting.” We treat money differently depending on where it is and what we call it.

Why You Should Name Your Savings Accounts

If you have a generic account called “Savings,” it is easy to dip into it for a weekend getaway. However, if that account is named “Down Payment for First Home” or “Daughter’s College Fund,” you are much less likely to “steal” from it. The emotional weight of the name acts as a barrier to impulsive spending.

Creating “Friction” for Spending

In 2026, technology has made spending frictionless. With biometric “Face-Pay” and one-click checkouts, the “pain of paying” has been almost entirely removed. To counter this, you must create intentional friction:

- Remove your credit card information from auto-fill on your browser.

- Delete shopping apps from your phone, forcing yourself to log in via a desktop.

- Implement a “24-Hour Rule”: For any purchase over $100, you must wait 24 hours before hitting the “buy” button.

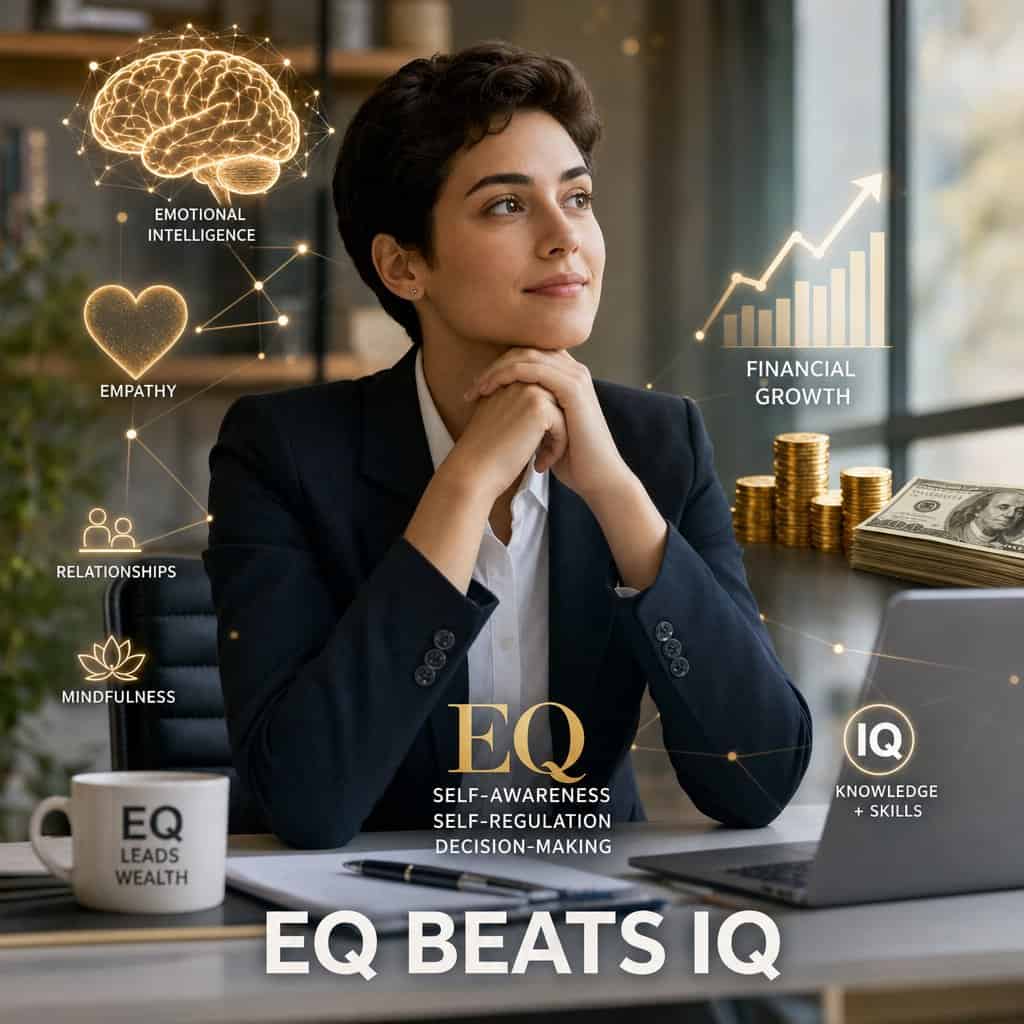

The Emotional Intelligence (EQ) of Wealth: Why EQ Beats IQ

In the world of finance, many people assume that the smartest person in the room—the one who can calculate complex derivatives or predict market swings—will be the wealthiest. History proves otherwise. Wealth is often captured by those with high Emotional Intelligence (EQ).

Delayed Gratification: The Ultimate Superpower

The ability to resist a small reward now in exchange for a much larger reward later is the single greatest predictor of financial success. In 2026, everything is designed to be “instant.” Instant streaming, instant delivery, and instant credit. By practicing delayed gratification, you are essentially opting out of the “poverty traps” that catch most of the population.

Managing the “Fear and Greed” Cycle

The market will fluctuate. In 2026, we may see volatility in tech sectors or shifts in global trade. A person with high EQ does not panic-sell when the market dips, nor do they “FOMO-buy” when a speculative asset is at its peak. They stay the course, trusting the automated systems and the diversified strategies laid out in this series.

Practical Implementation: Your 2026 Wealth-Builder Checklist

To move from theory to reality, follow this step-by-step checklist based on the principles of behavioral psychology and lifestyle management:

- Calculate Your “True” Income: Look at your take-home pay after taxes and mandatory deductions. This is your starting point.

- Identify Your “Big Three” Expenses: Housing, transportation, and food usually make up 70% of spending. Look for one way to optimize these (e.g., switching to a more fuel-efficient vehicle or meal-prepping).

- Set Up the “50% Raise Rule” Trigger: Contact your HR department or log into your payroll portal. Set it so that any future increases are automatically split between your checking and your high-yield savings account.

- Perform the “Subscription Slash”: Open your banking app right now. Scroll through the last 30 days. Identify three subscriptions you don’t use. Cancel them.

- Name Your Goals: Log into your HYSA and rename your sub-accounts. Give them names that stir emotion, like “Freedom Fund” or “Legacy Account.”

The Role of Community in Financial Success

Building wealth can be a lonely journey, especially if your social circle is prone to “conspicuous consumption” (spending money to show off). Finding a community of like-minded “Wealth-Builders” can provide the social reinforcement needed to stay disciplined. Whether it’s an online forum, a local investment club, or a professional financial coach, having someone to hold you accountable is invaluable.

Peer Accountability and the “Wealth Effect”

When you surround yourself with people who value financial independence over status symbols, your brain begins to normalize saving. You no longer feel like you are “missing out” when you skip a luxury purchase; instead, you feel a sense of pride in your growing “Freedom Fund.”

Funding a Future Where Work is Optional

Wealth isn’t built in a day; it’s built in the habits you repeat every month. By combining high-yield accounts, smart diversification, and a shield against lifestyle creep, you aren’t just saving money—you are funding a future where work is optional.

The 2026 Wealth-Builder Series is more than a set of instructions; it is a philosophy of intentional living. It is the recognition that every dollar you spend today is a piece of your freedom you are trading away. Conversely, every dollar you save and invest is a “worker” that will eventually earn money so you don’t have to.

As you move forward, remember that the goal isn’t to have the most money in the graveyard. The goal is to have the resources to live a life aligned with your values, to support the people you love, and to have the security to face whatever the future holds with confidence. You have the tools, you have the strategy, and now, you have the mindset. It’s time to build.

Frequently Asked Questions (FAQs)

Is lifestyle creep always a bad thing?

Not necessarily. Improving your quality of life as you work harder is a natural part of professional growth. The problem arises when your lifestyle grows faster than your savings. As long as you are following the 50% Raise Rule, you can enjoy your success guilt-free.

How do I know if I have “digital leaks”?

Check your bank statement for “micro-transactions.” If you see multiple charges under $15 that you don’t recognize or haven’t used recently, those are leaks. Many modern banking apps now have a “Subscription” tab that aggregates these for you.

Why is the 2026 Wealth-Builder Series focused so much on automation?

Automation removes “decision fatigue.” Every time you have to manually move money into savings, you are giving your brain a chance to talk you out of it. By automating, you ensure that your goals are met before your impulses can interfere.

Can I really build wealth with just $100 a month?

Yes. The most important factor in wealth building is not the amount, but the consistency and the time the money has to compound. Starting with $100 a month in a high-yield savings account or a diversified index fund creates a “habit of success.” In the 2026 Wealth-Builder Series, we emphasize that your behavior is the engine. As your income grows, that $100 will naturally scale into $500 or $1,000, but only if the foundational habit is already in place.

What should I do if I am already struggling with debt?

If you have high-interest debt (like credit cards), that is a “wealth-builder in reverse.” The interest you pay is someone else’s profit. We recommend a “Hybrid Approach”: continue a small automated transfer to your emergency fund (to prevent more debt when emergencies happen) while aggressively using the “Debt Snowball” or “Debt Avalanche” method to clear your balances. Once the debt is gone, redirect those monthly payments directly into your investment accounts.

How often should I review my automated systems?

We recommend a quarterly “Financial Health Check.” Every three months, sit down for 30 minutes to review your account balances, check for new digital leaks, and see if your interest rates on your high-yield savings accounts are still competitive. In the fast-moving economy of 2026, banks often update their rates, and you want to ensure your money is always working in the highest-performing environment possible.

Is it too late to start the 2026 Wealth-Builder Series if I’m behind?

It is never too late to take control of your financial future. The principles of compound interest and behavioral discipline work regardless of your age. While someone starting in their 20s has the advantage of time, someone starting in their 40s or 50s often has the advantage of higher earning potential. The goal is to maximize the resources you have now to fund the future you want later.

If you are ready to take the next step in your financial journey, explore our other articles in the series or create visual trackers for your savings goals.

Series Part 4: The Silent Wealth Killer: Defeating Lifestyle Creep in 2026

SERIES PART 5. MASTER MINDSET SHIFTS FOR FINANCIAL SUCCESS, DEFEAT LIFESTYLE CREEP, APPLY THE 50% RAISE RULE, AND AUDIT DIGITAL LEAKS WITH THE 2026 WEALTH-BUILDER SERIES TO FUND YOUR FUTURE.

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We don’t offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized advice. Track your progress for a better credit journey.

Written content – “Please view our full AI Use Disclosure.

“We improve our products and advertising by using Microsoft Clarity to see how you use our website. By using our site, you agree that we and Microsoft can collect and use this data. Our privacy policy has more details.”