11+ Proven Steps Millennials Can Master To Build Excellent Credit. Find Out More In Our Latest Article!

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

Don’t Have Time To Read The Full Article. Here’s What You Are Missing.

- 11+ Proven Steps Millennials Can Master To Build Excellent Credit. Find Out More In Our Latest Article!

- Understanding Credit Scores

- Importance of Good Credit

- Step 1: Checking Your Credit Report

- Step 2: Paying Bills on Time

- Step 3: Reducing Debt

- Step 4: Diversifying Your Credit

- Step 5: Avoiding New Debt

- Step 6: Maintaining Old Credit Accounts

- Step 7: Limiting Credit Inquiries

- Step 8: Addressing Credit Report Errors

- Step 9: Building Credit with Credit Cards

- Step 10: Using Installment Loans to Build Credit

- Step 11: Seeking Professional Help

- Maintaining Excellent Credit

- Frequently Asked Questions

Building excellent credit is crucial for millennials as they navigate their financial journey. A strong credit history with robust scores opens doors to favorable interest rates, better loan terms, and increased economic opportunities.

Whether you’re just starting your credit journey or looking to improve your scores, the following 11 proven steps can guide millennials toward establishing and maintaining excellent credit.

To build excellent credit, millennials need to understand the factors that affect their credit scores and take steps to improve them.

Understanding Credit Scores

A credit score is a three-digit number that represents an individual’s creditworthiness. Lenders use it to determine the likelihood of an individual repaying their debts on time.

The higher the credit score, the more likely an individual will be approved for credit and offered favorable terms and interest rates.

Credit scores are calculated based on several factors, including an individual’s payment history, credit utilization, length of credit history, types of credit used, and recent credit inquiries.

Payment history and credit utilization are the two most essential factors in determining a credit score, accounting for 35% and 30% of the score, respectively.

Payment history refers to an individual’s track record of making timely payments. Late payments, missed payments, defaults, and the negative after effects that occur such as liens, judgements, and collections can all negatively impact a credit score.

On the other hand, consistently making payments on time can help improve a credit score over time.

Credit utilization refers to the amount of credit an individual uses compared to their available credit. High credit utilization can indicate that an individual relies too heavily on credit and may be at risk of defaulting on their debts.

Lenders prefer low credit utilization, ideally below 30% of available credit.

Millennials need to understand how credit scores work and how they are calculated. By maintaining a solid payment history, keeping credit utilization low, and being mindful of other factors that impact credit scores, millennials can build excellent credit and set themselves up for financial success.

Importance of Good Credit

Good credit is crucial for millennials who want financial stability and independence.

A good credit score opens various financial and economic opportunities, such as getting approved for loans, credit cards, and mortgages, with lower interest rates and better terms.

It also reflects positively on one’s financial responsibility and management skills, leading to better job prospects, lower insurance premiums, and even rental approvals.

On the other hand, having bad credit can limit one’s financial options, making it harder to secure loans, credit, and even rental agreements.

It can also result in higher interest rates, leading to more debt and financial stress. Therefore, millennials must understand the importance of building and maintaining good credit.

One way to build good credit is by paying bills on time, as payment history is the most significant factor in credit scores.

Millennials can also benefit from keeping their credit utilization low, which means not maxing out their credit cards and paying balances in full each month.

Additionally, they can benefit from having a mix of credit types, such as credit cards, auto loans, and student loans, which shows that they can handle different types of debt responsibly.

Good credit is essential for millennials who want to achieve financial success. It can open doors to various economic opportunities, while bad credit can limit one’s options and lead to financial stress. By following the proper steps and building good credit, millennials can set themselves up for a brighter financial future.

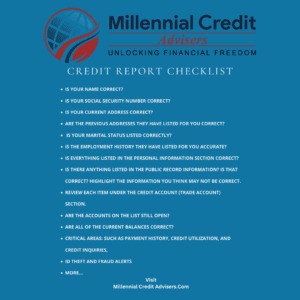

Step 1: Checking Your Credit Report

The first step in building excellent credit is to check your credit report. This report contains information about your credit history, such as your payment history, credit utilization, and any negative marks on your credit.

By checking your credit report, you can ensure that all the information is accurate and up-to-date.

There are three major credit agencies: Equifax, Experian, and TransUnion. You are entitled to a weekly free credit report from each agency once a year. To get your free credit report, go to AnnualCreditReport.com.

Once you have your credit report, please review it carefully for errors or inaccuracies. If you find any errors, you can dispute them with the credit agency. This can help improve your credit score if the error is corrected.

In addition to checking for errors, reviewing your credit report can help you identify areas where you need to improve your credit. For example, if you have a high credit utilization rate, you may need to pay down your debt to improve your credit score.

Checking your credit report is an essential first step in building excellent credit. By ensuring the information is accurate and up-to-date, you can take the necessary steps to improve your credit score and build a strong credit history.

Step 2: Paying Bills on Time

One of the most critical factors in building excellent credit is paying bills on time. Late payments can significantly impact your credit score and stay on your credit report for up to seven years.

Setting up reminders and creating a system to ensure all bills are paid on time is essential to avoid late payments. This can include setting up automatic payments or using a calendar or app to keep track of due dates.

It’s also essential to prioritize and pay bills in order of importance. For example, paying rent or mortgage payments on time is crucial as they are often the most significant monthly expenses. Other vital bills to prioritize include utilities, car payments, and credit card bills.

Consider creating a budget and tracking expenses to make it easier to keep track of bills and due dates. This can help you stay on top of bills and avoid overspending.

Paying bills on time is a crucial step in building excellent credit. By setting up reminders, prioritizing bills, and tracking expenses, millennials can establish a strong credit history and improve their credit score.

Step 3: Reducing Debt

Reducing debt is an essential step to building excellent credit for Millennials. High credit utilization can significantly impact credit scores, so keeping debt levels low is crucial. Here are some practical ways to reduce debt:

- Create a realistic budget.

Creating a realistic budget is the first step towards reducing debt. It helps you identify areas where you can cut back on expenses and allocate more funds towards paying off debt. Use a budgeting app or spreadsheet to track your income and expenses and identify areas where you can save money.

- Prioritize high-interest debt

High-interest debt, such as credit card debt, can quickly spiral out of control if left unchecked. Prioritize paying off high-interest debt first, as it will save you money in the long run. Consider consolidating high-interest debt into a lower-interest loan or balance transfer credit card.

- Negotiate with creditors

If you’re struggling to make payments, consider negotiating with your creditors. They may be willing to work out a payment plan or reduce your interest rate. Be honest about your financial situation and explain your willingness to pay off the debt.

- Avoid taking on new debt

Avoid taking on new debt while you’re trying to reduce existing debt. It’s essential to break the cycle of debt and avoid high credit utilization. Consider using cash or a debit card instead of a credit card.

By reducing debt, Millennials can improve their credit utilization and build excellent credit over time. It takes time and effort, but the payoff is worth it.

Step 4: Diversifying Your Credit

Once you have established a good credit history with an entry-level credit card, it’s time to diversify your credit. Diversifying your credit means having different types of credit accounts, such as a car loan, a student loan, or a mortgage.

A mix of credit accounts can positively impact your credit score by showing lenders that you can responsibly manage different types of credit. According to CNBC, “Credit mix accounts for 10% of your FICO score, and lenders like to see that you can handle different types of credit.”

Here are some ways to diversify your credit:

- Apply for a car loan: If you need a car, consider getting a car loan. The vehicle secures This type of loan, and you make monthly payments until the loan is paid off.

- Apply for a student loan: If you’re still in school or recently graduated, consider getting a student loan. This type of loan can help you pay for tuition, books, and other education-related expenses.

- Apply for a mortgage: If you’re ready to buy a house, consider getting one. This type of loan is used to purchase a home and is secured by the property.

Remember to only apply for credit that you need and can afford. Applying for too much credit at once can negatively impact your credit score.

In addition to diversifying your credit, it’s important to continue practicing good credit habits, such as paying your bills on time and keeping your credit utilization low. By following these steps, millennials can build excellent credit and achieve their financial goals.

Step 5: Avoiding New Debt

One of the most critical steps in building excellent credit is avoiding new debt. Millennials should be cautious when taking on new debt, especially if they already have outstanding debt. New debt can lower their credit score and make it harder to pay off existing debt.

To avoid new debt, millennials must create and stick to a budget. This means only spending money on essential items and avoiding unnecessary purchases. They should also avoid using credit cards to make purchases they cannot afford to pay off immediately.

Another way to avoid new debt is to pay off existing debt immediately. This means making more than the minimum monthly payment and paying off high-interest debt first. By reducing their overall debt, millennials can improve their credit score and make it easier to avoid new debt.

Millennials should be cautious when applying for new credit. Each time they apply for credit, it can lower their credit score. They should only apply for credit when needed and are confident they will be approved. They should also avoid applying for multiple types of credit at once, which can lower their credit score.

Avoiding new debt is a crucial step in building excellent credit. Millennials should be cautious with spending, pay off existing debt, and be careful when applying for new credit. Following these steps can improve their credit score and achieve financial success.

Step 6: Maintaining Old Credit Accounts

Maintaining old credit accounts is essential in building excellent credit for millennials. When you close a credit account, you lose the credit history associated with it, which can negatively impact your credit score. Therefore, it is recommended that you keep your oldest credit accounts open, even if you no longer use them.

One way to maintain old credit accounts is to use them occasionally. For example, you can charge a small purchase to an old credit card and pay it off monthly. This will keep the account active and show you are responsible with credit.

Another critical aspect of maintaining old credit accounts is to monitor them regularly. Check your credit report at least twice yearly to ensure all the information is accurate and up-to-date. If you notice any errors, dispute them immediately with the credit agency.

It is also essential to keep your contact information up-to-date with your creditors. If your address or phone number changes, update your information with creditors to ensure you receive important notifications and bills.

Maintaining old credit accounts is crucial in building excellent credit for millennials. By keeping your most aged credit accounts open, using them occasionally, monitoring them regularly, and updating your contact information, you can ensure that you have a strong credit history to help you achieve your financial goals.

Step 7: Limiting Credit Inquiries

When a lender checks an individual’s credit report, it is called a “hard inquiry.” Hard inquiries can negatively affect a credit score, especially if there are multiple inquiries within a short period. Therefore, it is essential to limit credit inquiries as much as possible.

One way to limit credit inquiries is to only apply for credit when necessary. Millennials should avoid applying for multiple credit cards or loans simultaneously, as this can lead to multiple hard inquiries on their credit report. Instead, they should research and compare different credit products before applying for one that best suits their needs.

Another way to limit credit inquiries is to use pre-approval offers. Pre-approval offers allow individuals to see if they qualify for a credit product without a hard inquiry. This can help millennials avoid unnecessary hard inquiries on their credit report.

Millennials should regularly monitor their credit report to ensure no unauthorized hard inquiries. They should dispute any unauthorized inquiries with the credit agency immediately if they notice any unauthorized inquiries.

By limiting credit inquiries, millennials can protect their credit score and increase their chances of being approved for credit products in the future.

Step 8: Addressing Credit Report Errors

Even when you are careful with your credit, errors can still occur on your credit report. Inaccurate information on your credit report can negatively impact your credit score, so it is essential to address any errors immediately.

The first step in addressing credit report errors is to obtain a copy of your credit report from each of the three major credit reporting agencies: Equifax, Experian, and TransUnion. You are entitled to one free copy of your credit report from each agency every 12 months, and you can request your reports from AnnualCreditReport.com.

Once you have your credit reports, review them carefully for any errors. Common errors include incorrect personal information, accounts that belong to someone else, and incorrect account balances. If you find any errors, you should dispute them with the credit reporting agency that issued the report.

To dispute an error on your credit report, you should write a letter to the credit reporting agency that issued the report. In the letter, explain the error and provide any supporting documentation you have. The credit reporting agency is required to investigate the dispute and respond to you within 30 days.

If the credit reporting agency does not correct the error, you can also dispute the error with the creditor that provided the inaccurate information. The creditor must also investigate the dispute and respond to you within 30 days.

Addressing credit report errors can take time, but it is essential to maintain good credit. Regularly reviewing your credit reports and addressing any errors can ensure that your credit score accurately reflects your credit history and financial responsibility.

Step 9: Building Credit with Credit Cards

Credit cards can be a powerful tool for building credit and a double-edged sword. Credit cards can quickly lead to debt and damage your credit score if used irresponsibly. However, if used correctly, credit cards can help you build a positive credit history and improve your credit score.

One of the most important things to remember when using credit cards to build credit is always making your payments on time. Late payments can significantly negatively impact your credit score and stay on your credit report for up to seven years.

Another critical factor to consider is your credit utilization ratio, which is the amount of credit you’re using compared to the amount of available credit. Keeping your credit utilization ratio below 30% is generally recommended to avoid damaging your credit score.

In addition to making timely payments and keeping your credit utilization ratio low, you can use several other strategies to build credit with credit cards. These include:

- Applying for a secured credit card: A secure credit card requires you to make a deposit, which serves as collateral for your credit limit. This can be a good option if you have little or no credit history.

- Becoming an authorized user: If you have a family member or friend with good credit, you can ask them to add you as an authorized user on their credit card. This can help you build credit without taking on any debt.

- Applying for a student credit card: Many credit card companies offer cards specifically designed for college students. These cards often have lower credit limits and more lenient approval requirements, making them a good option for young people with limited credit history.

Credit cards can be a valuable tool for building credit, but it’s essential to use them responsibly and avoid taking on more debt than you can handle. By following these tips and using credit cards wisely, you can build a strong credit history and improve your credit score.

Step 10: Using Installment Loans to Build Credit

Installment loans are a type of loan repaid over a set period in regular installments. They are an excellent option for building credit because they show lenders that you can manage debt responsibly.

When using installment loans to build credit, it’s essential to make sure you choose a loan that you can afford to repay. Late or missed payments can hurt your credit score.

One way to use installment loans to build credit is to take out a small personal loan and make timely payments. This can show lenders that you are responsible with debt and can help improve your credit score.

Another option is to take out a secured loan backed by collateral such as a car or house. Secured loans can be easier to qualify for and may have lower interest rates, but they also come with the risk of losing your collateral if you default on the loan.

It’s essential to shop around and compare rates and terms from different lenders before choosing an installment loan. Look for lenders that report to the major credit agencies, which will help ensure your payments are reflected on your credit report.

Using installment loans to build credit can be an effective strategy for millennials looking to establish or improve their credit history. By making payments on time and choosing a loan that fits their budget, they can demonstrate their creditworthiness and improve their chances of being approved for future loans and credit cards.

Step 11: Seeking Professional Help

Building credit can be daunting, especially if you are new to it. Seeking professional help can be a great way to ensure you are on the right track. Many professionals, including credit counselors, financial advisors, and credit repair companies, can help you with credit building.

Credit counselors can help you create a budget and develop a plan to pay off your debts. They can also advise you on how to improve your credit score.

Financial advisors can help you create a long-term financial plan with credit building. They can also help you invest your money wisely and manage your finances.

Use credit repair companies as a last resort or choice. credit repair companies advertise that they can help you fix errors on your credit reports and improve your credit scores. However, it is essential to do your research before choosing a credit repair company. Some companies may charge high fees and make false promises.

Before seeking professional help, it is essential to do your research and choose a reputable professional. Look for professionals who are licensed, experienced, and have a good reputation. You can also ask for recommendations from friends and family members.

Seeking professional help can be a great way to ensure you are on the right track to building excellent credit. Whether you work with a credit counselor, financial advisor, or credit repair company, choosing a reputable professional and doing your research is essential. With the right help and guidance, you can achieve your credit goals and build a strong financial future.

Maintaining Excellent Credit

Building excellent credit takes time, discipline, and effort. However, maintaining excellent credit is equally important. Once you have built a good credit score, you must continue using credit responsibly to keep your score high. Here are some final tips to help you maintain excellent credit:

Pay Your Bills on Time

One of the most crucial factors in maintaining excellent credit is paying your bills on time. Late payments can have a significant negative impact on your credit score. Therefore, it is essential to make sure you pay your bills on time, every time. Consider setting up automatic payments or reminders to help you stay on track.

Keep Your Credit Utilization Low

Another critical factor in maintaining excellent credit is keeping your credit utilization low. This means using only a small percentage of your available credit. A good guideline is to use less than 30% of your limit on any given credit card. High credit utilization can negatively impact your credit score, so it’s essential to keep it low.

Monitor Your Credit Report

Regularly monitoring your credit report can help you identify any errors or fraudulent activity that may negatively impact your credit score. You are entitled to one annual free credit report from each national credit agency. Review your report carefully and dispute any errors or inaccuracies you find.

Practice Responsible Credit Habits

Finally, it is essential to practice responsible credit habits to maintain excellent credit. This means only applying for credit when needed, avoiding opening too many accounts simultaneously, and keeping your balances low.

By following these 11 proven steps, millennials can lay the foundation for excellent credit, paving the way for a more secure financial future. Building and maintaining good credit habits opens up economic opportunities and establishes a solid financial reputation for many years.

Frequently Asked Questions

What are some effective ways to start building credit as a millennial?

One effective way to start building credit as a millennial is to apply for a credit card and use it responsibly. Another way is to become an authorized user on someone else’s credit card account. Additionally, paying bills on time and low credit utilization can help build credit.

How long does it typically take to achieve a good credit score?

Achieving a good credit score can take time, typically at least a few months to a year of responsible credit use. However, it can take longer for those with a limited credit history.

What are some common mistakes to avoid when building credit?

Some common mistakes to avoid when building credit include missing payments, applying for too many credit accounts at once, and maxing out credit cards. It is also important to monitor credit reports for errors and fraudulent activity.

Can you improve your credit score quickly, and if so, how?

While improving a credit score quickly is possible, it typically requires a significant effort. One way to do this is to pay down credit card balances to decrease credit utilization. Disputing errors on credit reports and negotiating with creditors can help improve a credit score.

What are some strategies for maintaining a good credit score over time?

To maintain a good credit score over time, it is essential to continue using credit responsibly, paying bills on time, and keeping credit utilization low. Additionally, regularly monitoring credit reports and addressing any errors or fraudulent activity can help maintain a healthy credit score.

How can you monitor your credit score and ensure that it stays healthy?

There are several ways to monitor credit scores and ensure they stay healthy. One way is to regularly check credit reports from the three major credit agencies. Some credit card companies and financial institutions also offer free credit monitoring services. It is also essential to immediately address any errors or fraudulent activity on credit reports.

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We don’t offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized advice. Track your progress for a better credit journey.

Written content – “Please view our full AI Use Disclosure.”

We improve our products and advertising by using Microsoft Clarity to see how you use our website. By using our site, you agree that we and Microsoft can collect and use this data. Our privacy policy has more details.