The Top 12 Credit Report Errors You Should Look for. Find Out More In Our Latest Article!

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

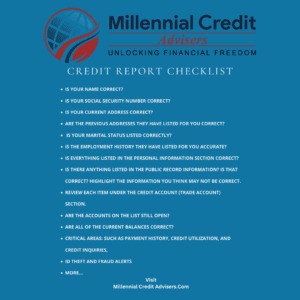

Don’t Have Time To Read The Full Article. Here’s What You Are Missing.

Security hacks seem to occur daily, with the most recent possibly being a social security number breach affecting over 2.9 billion individuals. When uncommon errors such as identity theft occur, they can be costly for all concerned parties.

Is the credit information in your credit reports accurate or inaccurate?

You may never know if you’re not evaluating, auditing, and reviewing your credit reports!

Why does triple-checking your credit reports and credit scores matter?

If your credit has been established for some time or you have accounts that are currently open and active, often, you don’t think about your credit reports having any problems.

Problems could happen. If it’s been a while since you last reviewed or looked at your credit reports. You may never know.

It’s also best to triple check your credit reports and scores from all Three major credit reporting companies.

When perusing your credit reports. Be sure to look for information that may be erroneous, inaccurate, incomplete, incorrect, or unknown.

Take a peek at some of the most listed types of errors you can quickly check to make sure your credit reports are accurate and up-to-date:

According to major credit reporting companies, the Consumer Financial Protection Bureau and specialty reporting agencies, here’s a list of types of important information and errors you can quickly look for.

Personal information

- Errors in your identity data, such as wrong name, phone number, or address

- Accounts belonging to another person with the same or similar name as yours

- Incorrect accounts resulting from identity theft

Reporting of account status

- Closed accounts reported as open

- You’re reported as the account owner when you’re just an authorized user.

- Accounts that are incorrectly reported as late or delinquent

- Incorrect date of last payment, date opened, or date of first delinquency

- The same debt listed more than once

Balance errors

- Accounts with incorrect current balance

- Accounts with an incorrect credit limit

Data management errors

- Reinsertion of incorrect information after it was corrected

- Accounts that appear multiple times with different creditors listed

Of course, this isn’t a final list. But it’s a great place to start. Look for anything different and anything you’re unaware of.

If you have any problems, contact all the national credit reporting agencies.

I recommend requesting your free credit reports from annualcreditreport.com at least once a year.

Order your Three bureau credit reports from Equifax, Experian and TransUnion at least four times a year (Credit data changes quickly) or two times a year at a minimum. The best way to monitor your credit reports.

If there are problems, contact all the credit reporting agencies using their dispute portal and process.

How to dispute Equifax credit report

How to dispute Experian credit report

How to dispute TransUnion credit report

| EQUIFAX | EXPERIAN | TRANSUNION |

| Online Credit Dispute: Equifax credit report | Online Credit Dispute: Experian credit report | Online Credit Dispute: TransUnion credit report |

| By phone: Phone number provided on credit report or (800) 864-2978 | By phone: Phone number provided on credit report or (888) 397-3742 | By phone: (800) 916-8800 |

| Equifax Information Services, LLC P.O. Box 740256 Atlanta, GA 3037 | Experian P.O. Box 4500 Allen, TX 75013 | TransUnion LLC Consumer Dispute Center P.O. Box 2000 Chester, PA 19016 |

If your accounts have been established for many years, you’ve recently established credit, or you’re applying for credit for the first time.

Order your credit reports & continue to regularly evaluate, audit, and review your credit reports for errors, inaccurate, incomplete, incorrect, and unknown information.

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We don’t offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized advice. Track your progress for a better credit journey.

Written content – “Please view our full AI Use Disclosure.

We improve our products and advertising by using Microsoft Clarity to see how you use our website. By using our site, you agree that we and Microsoft can collect and use this data. Our privacy policy has more details.”