Kickstart Your Ultimate Savings Challenge for Unmatched Long-Term Success! Find Out More In Our Latest Article!

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

DON’T HAVE TIME TO READ THE FULL ARTICLE. HERE’S WHAT YOU ARE MISSING.

- Setting Your Savings Goals

- Assess Your Financial Situation

- Define Clear, Achievable Goals

- Creating a Budget

- Track Your Spending

- Prioritize Expenses

- Plan for Non-Monthly Expenses

- Choosing the Right Savings Tools

- High-Interest Savings Accounts

- Certificates of Deposit

- Automatic Transfers

- Cutting Unnecessary Costs

- Eliminate Impulse Purchases

- Reduce Monthly Subscriptions

- Monitoring Progress and Adjusting Strategies

- Regularly Review Your Budget

- Adapt to Financial Changes

- Frequently Asked Questions

Starting a savings challenge can be daunting, but with the right mindset and strategies, it can be a rewarding experience that leads to long-term financial success.

Whether saving for a down payment on a house, creating an emergency fund, or simply looking to improve your financial health, a savings challenge can help you achieve your goals.

To ensure optimal long-term success, approach your savings challenge with a clear plan and the right tools.

This article provides tips for starting your ultimate savings challenge, including setting your savings goals, creating a budget, choosing the right savings tools, cutting unnecessary costs, monitoring progress, and adjusting strategies.

By following a few tips, you can create a savings challenge tailored to your unique financial situation and goals and set yourself up for long-term economic success.

Whether you are a seasoned saver or just starting, these tips will help you take control of your finances and achieve your financial goals.

Setting Your Savings Goals

Assess Your Financial Situation

Before setting your savings goals, assessing your current financial situation – including income, expenses, and debts- is essential. Understanding your financial standing can help you set realistic and achievable savings goals.

One way to assess your financial situation is to create a budget. This can help you identify areas for reducing expenses and allocating more money to savings. Many budgeting tools, such as YNAB, EveryDollar, and Empower, are available online.

Another essential aspect to consider is debt. If you have high-interest debt, such as credit card debt, it may be beneficial to focus on paying it off before allocating a large portion of your income to savings.

Define Clear, Achievable Goals

Once you have assessed your financial situation, it’s time to define clear and achievable savings goals. Setting specific and measurable goals, such as saving a certain amount each month or saving for a particular expense, like a down payment on a house or a vacation, is essential.

Consider setting deadlines for each goal to help you stay motivated. This can help you stay on track and ensure that you are making progress toward your savings goals.

It’s also essential to make sure that your goals are achievable. If you set unrealistic goals, you may become discouraged and give up on your savings journey. Start small and gradually increase your savings goals as you become more comfortable with saving.

By assessing your financial situation and setting clear, achievable goals, you can set yourself up for long-term savings success.

Creating a Budget

Creating a budget is the first step towards financial freedom. It helps you understand where your money is going and where you can cut back. Establish your budget in five easy steps that suit your needs.

Track Your Spending

The first step in creating a budget is tracking your spending. This will help you understand where your money is going and where you can cut back. You can use a spreadsheet or a budgeting app to track your spending. Be sure to categorize your expenses, such as rent, utilities, groceries, entertainment, etc.

This will help you identify areas where you are overspending.

Prioritize Expenses

Once you have tracked your spending, it’s time to prioritize your expenses. List your essential expenses, such as rent, utilities, and groceries. Then, list your discretionary expenses, such as entertainment and dining out. Prioritize your necessary expenses and look for ways to reduce your discretionary expenses.

Plan for Non-Monthly Expenses

One of the biggest challenges of budgeting is planning for non-monthly expenses, such as car repairs and medical bills. To avoid being caught off guard, create a sinking fund—a separate savings account for these expenses. Divide the total cost of the expense by the number of months until it’s due, and save that amount each month.

Following these tips can help you create a budget that works for you and enables you to achieve your financial goals.

Choosing the Right Savings Tools

When it comes to saving money, choosing the right savings tools can make a big difference in achieving long-term success. Here are three popular savings tools to consider:

High-Interest Savings Accounts

High-interest savings accounts are an excellent option for those who want to earn interest on their savings while still having easy access to their money. These accounts typically offer higher interest rates than traditional savings accounts, which means you can earn more money on your balance over time. Some popular high-interest savings accounts include Ally Bank’s Online Savings Account and Discover’s Online Savings Account.

Certificates of Deposit

Certificates of Deposit (CDs) are another savings tool to consider. CDs are savings accounts that allow you to earn a fixed interest rate over a set period. This means you can lock in a higher interest rate than you would with a traditional savings account. However, the downside is that you won’t be able to access your money until the CD reaches maturity. Some popular CDs include Marcus by Goldman Sachs’ High-Yield CD and Barclays’ Online CD.

Automatic Transfers

One of the easiest ways to save money is to set up automatic transfers from your checking account to your savings account. This way, you don’t have to think about saving money – it happens automatically. You can set up automatic transfers weekly, bi-weekly, or monthly, depending on your needs.

Some banks even offer automatic savings plans that round up purchases to the nearest dollar and deposit the difference into your savings account.

Automatic savings accounts are a great way to save money without realizing it.

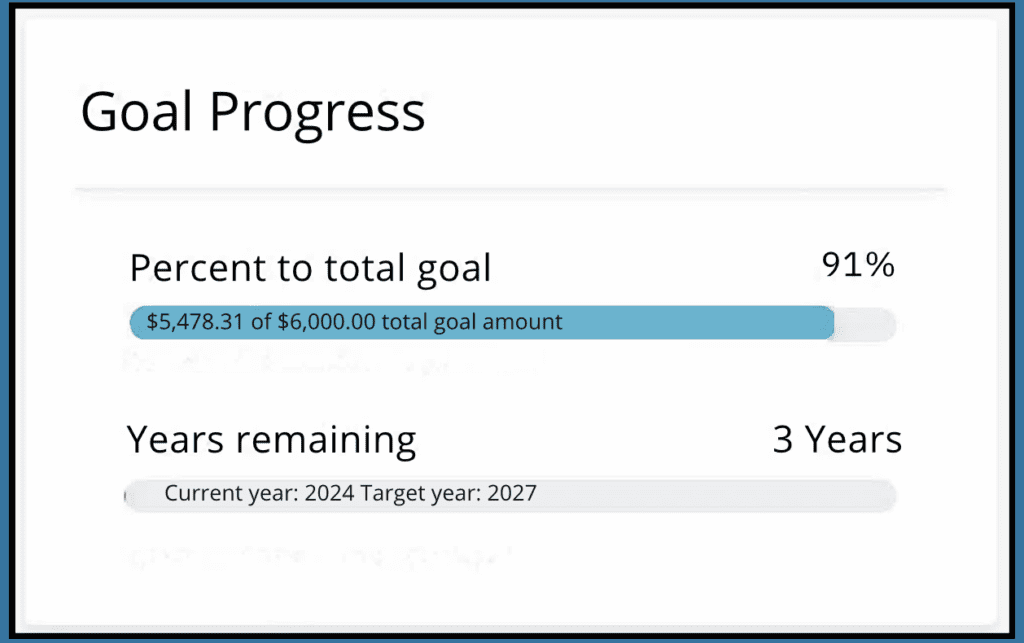

Here’s a peek at how one individual’s automatic savings goal started with very little discretionary income each month and now has more than enough to cover their high-mileage-driven vehicle maintenance repairs.

No matter if you’re saving $6,000.00, $60,000.00 or $6,000,000.00. Automating your savings accounts is a great way to save money without realizing it. Pass it on!

Before you pass it on, be the next individual to win your savings challenge! Your first win is an easy one. Start saving today!

Ultimately, the right savings tools depend on your needs and financial goals. When choosing a savings tool, consider your goals and how much risk you’re willing to take. With the right tools and strategies, you can start your ultimate savings challenge and achieve long-term success.

Cutting Unnecessary Costs

Cutting unnecessary costs is an essential part of any savings challenge. Reducing expenses can free up more money for your savings goals. Here are some tips to help you cut unnecessary costs:

Eliminate Impulse Purchases

Impulse purchases can quickly add up and derail your savings challenge. List what you need before shopping to avoid impulse purchases and stick to it. Also, consider waiting 24 hours before purchasing to determine if it is a necessity or a want.

Another way to reduce impulse purchases is to unsubscribe from marketing emails and avoid browsing online shopping sites. If you need to make a purchase, consider buying used or refurbished items instead of new ones.

Reduce Monthly Subscriptions

Monthly subscriptions can also eat away at your savings. Look at your monthly bills and identify subscriptions you no longer use or need. Canceling these subscriptions can save you a significant amount of money each month.

Consider negotiating with service providers for a better rate or switching to a cheaper alternative. For example, if you have a gym membership, consider canceling it and working out at home or outside. Alternatively, you can switch to a cheaper gym or fitness program.

You can free up more money towards your savings goals by cutting unnecessary costs. Keep track of your progress and adjust your budget as needed to ensure you stay on track.

Monitoring Progress and Adjusting Strategies

To ensure the success of your ultimate savings challenge, monitoring your progress and adjusting your strategies regularly is essential. Here are some tips to help you stay on track:

Regularly Review Your Budget

Regularly reviewing your budget is one of the most critical steps in monitoring your progress. This will help you identify areas where you may be overspending or where you can cut back. By keeping track of your income and expenses, you can make informed decisions about where to allocate your funds and adjust your savings strategies as needed.

Consider creating a spreadsheet or using a budgeting app to track your expenses. This will help you see where your money is going and identify areas for improvement. Be sure to review your budget regularly, such as weekly or monthly, to stay on top of your progress.

Adapt to Financial Changes

It is also essential to be flexible and adapt your savings strategies to any financial changes. For example, you should increase your savings goals if you receive a raise or bonus at work. On the other hand, if you experience a financial setback, such as an unexpected expense, you may need to adjust your budget and savings plan accordingly.

By regularly monitoring your progress and adapting to financial changes, you can stay on track with your savings goals and achieve long-term success. Remember, the key to success is consistency, patience, and flexibility.

Frequently Asked Questions

What are the best strategies for beginners to invest for long-term gains?

For beginners, the best investment strategy for long-term gains is to start with small amounts and gradually increase the investment over time. Diversification of assets is also essential to reduce risk. It is recommended that they invest in low-cost index funds or exchange-traded funds (ETFs) that track the stock market’s performance. A long-term perspective is also essential, as short-term market fluctuations can be unpredictable.

How can one effectively save money to fund future investments?

Creating and sticking to a budget is essential to effectively save money for future investments. One should prioritize saving a certain percentage of their monthly income before spending on discretionary items. Automating savings by setting up automatic transfers to a savings account is also helpful. Cutting back on unnecessary expenses and finding ways to increase income can also help to save more money.

Can you explain the 50/30/20 budgeting rule and how it applies to saving?

The 50/30/20 budgeting rule is a guideline for budgeting in which 50% of income is allocated to necessities, 30% to discretionary spending, and 20% to savings and debt repayment. This rule can help create a balanced budget and ensure that a portion of income is dedicated to savings. However, adjusting this rule based on individual circumstances and goals is essential.

What are the potential drawbacks of committing to long-term investments?

Committing to long-term investments can have potential drawbacks, including the risk of market fluctuations and the possibility of missing out on short-term gains. Additionally, long-term investments may not be suitable for everyone, as individual circumstances and goals may vary.

How can someone save a significant sum, such as $10,000, within a short timeframe?

To save a significant sum of money within a short timeframe, it is essential to set a specific goal and create a plan to achieve it. This may involve cutting back on unnecessary expenses, increasing income, and prioritizing savings over discretionary spending. It may also be helpful to consider short-term investments with higher risk and return potential.

What are some effective tips for beginners looking to invest in the stock market?

Some effective tips for beginners who want to invest in the stock market include starting small, diversifying investments, and having a long-term perspective. Researching and staying informed about market trends and developments is also essential. Working with a financial advisor or using a robo-advisor platform can also be helpful.

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We don’t offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized advice. Track your progress for a better credit journey.

Written content: Please view our full AI Use Disclosure.

We improve our products and advertising by using Microsoft Clarity to see how you use our website. By using our site, you agree that we and Microsoft can collect and use this data. Our privacy policy has more details.

{kind=link}

{kind=link}