How To Increase Credit Score Fast For Beginners: A Complete Guide to Building Better Credit. Find Out More In Our Latest Article.

THIS ARTICLE MAY CONTAIN AFFILIATE LINKS, MEANING I GET A COMMISSION IF YOU DECIDE TO MAKE A PURCHASE THROUGH MY LINKS AT NO COST TO YOU. PLEASE READ MY AFFILIATE DISCLOSURE FOR MORE INFO.

DON’T HAVE TIME TO READ THE FULL ARTICLE. HERE’S WHAT YOU ARE MISSING.

- How To Increase Credit Score Fast For Beginners: A Complete Guide to Building Better Credit. Find Out More In Our Latest Article.

- Next Steps visit Millennial Credit Advisers

- Start Improving Your Credit Score Today

- Understanding Credit Scores

- Quick Steps to Increase Your Credit Score Fast

- Building Healthy Credit Habits

- Advantages of Boosting Your Credit Score Quickly

- Disadvantages and Risks of Rapid Credit Score Increases

- Beginner Credit Tools and Resources

- Monitoring Your Credit Progress

- Key Giveaways

- Visit Millennial Credit Advisers

- Start Improving Your Credit Score Today

- Frequently Asked Questions

Building a strong credit score can feel overwhelming, especially if you’re just starting out. But with the right moves, you can boost your score in a matter of months, not years.

Some folks think improving credit takes forever. Actually, a few focused actions—like paying down balances, fixing errors, or becoming an authorized user on a responsible person’s account—can spark changes in 30 to 90 days.

Credit scores touch everything—renting an apartment, getting a car loan, sometimes even job offers. If you’re young or new to credit, it’s easy to feel stuck because you don’t have much history or maybe made a few rookie mistakes.

Knowing which steps matter most helps you focus your energy and see actual results. Don’t waste time on stuff that barely moves the needle.

Most beginners see progress by zeroing in on two things: payment history and credit utilization. These two make up 65% of your score.

Pay your bills on time and keep your card balances low. It’s basic, but honestly, these changes can give your score a real lift in just a few months.

Key Takeaways

- Payment history and credit utilization matter most for beginners

- Strategic debt paydown and error removal can spark improvement in 30-90 days

- Long-term credit health comes from steady habits: on-time payments, low usage

Understanding Credit Scores

Credit scores are just three-digit numbers showing how you handle debt and bills. They influence whether you get approved for loans, what interest rates you get, and sometimes even which apartments you can rent.

What Is a Credit Score?

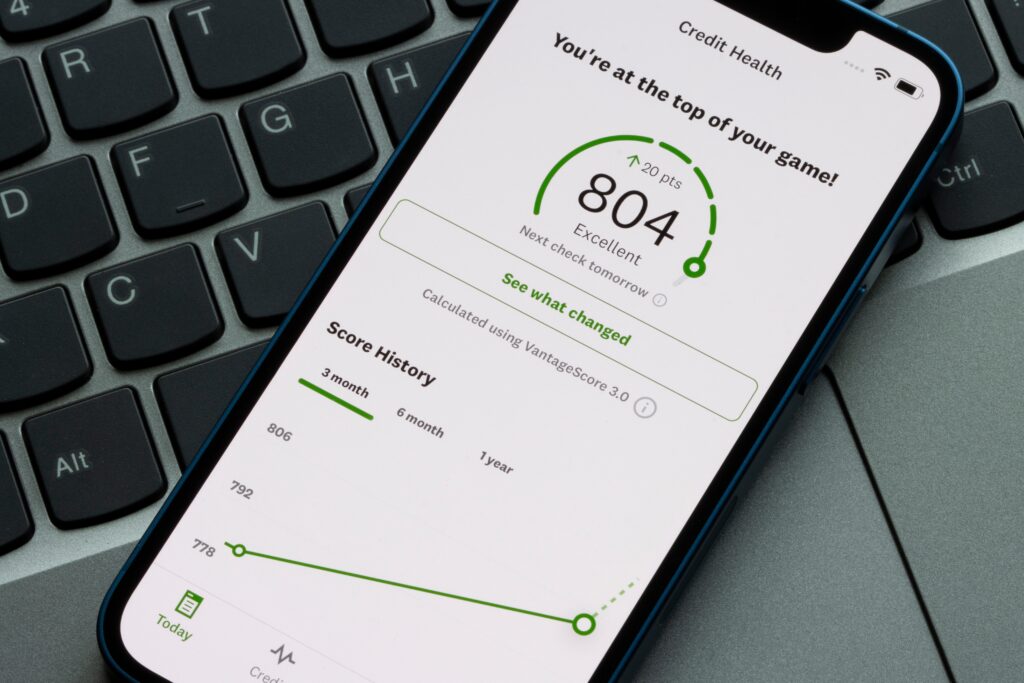

Your credit score falls somewhere between 300 and 850. Lenders use it to size up how risky it’d be to loan you money.

Higher numbers mean you’re less risky in their eyes. That’s the goal, right?

- Excellent: 800-850

- Very Good: 740-799

- Good: 670-739

- Fair: 580-669

- Poor: 300-579

Most lenders use FICO or VantageScore. Both use similar methods to crunch the numbers.

Credit scores shift every month as banks send in new info. One late payment can drop your score by 60 to 110 points.

Opening a new account can knock your score down by 5 to 10 points for a bit. It’s not forever, but it stings.

How Are Credit Scores Calculated?

Your score comes from five main factors. Each one counts for a different chunk of the total.

FICO Score Breakdown:

- Payment history: 35%

- Credit utilization: 30%

- Length of credit history: 15%

- Credit mix: 10%

- New credit inquiries: 10%

Payment history checks if you pay bills on time. Even one late payment (over 30 days) can hurt.

Credit utilization looks at how much of your available credit you’re using. If you keep your balances under 30% of your total limits, you’re in good shape. Under 10% is even better.

Length of credit history just means how long you’ve had accounts open. Older is better.

Why Credit Scores Matter for Beginners

Credit scores decide which financial products you can get and what rates you’ll pay. Good scores save you a lot of money, plain and simple.

Benefits of Higher Credit Scores:

- Lower interest rates on loans

- Better credit card offers

- Easier time renting apartments

- Lower insurance premiums

- Access to some jobs

If you have a 760 score, you might snag a 6% car loan. With a 620, you could pay 12% for the same car. Ouch.

Landlords check credit, too. Many want to see scores above 650 before handing over the keys.

Some jobs—especially those handling money or security—look at your credit report. Bad credit can close doors in banking or government work.

Start building good credit early and you’ll have more options later. It’s a head start that really pays off when it’s time to buy a home or launch a business.

Quick Steps to Increase Your Credit Score Fast

Let’s get to the good stuff. These three steps can make a difference fast, sometimes in just 30-60 days. Focus on removing errors, paying bills on time, and keeping your credit card balances in check.

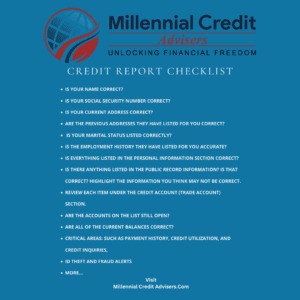

Check Your Credit Report for Errors

Millions of Americans have credit report mistakes dragging down their scores. You can grab free reports once a year from each big bureau at AnnualCreditReport.com.

Common issues? Wrong account info, payments marked late when you paid on time, or accounts that aren’t even yours. Sometimes other people’s data gets mixed in—super frustrating.

The dispute process goes through each bureau separately. You can file disputes online, by mail, or over the phone. Disputing errors can wipe out negative marks pretty quickly.

The bureaus get 30 days to check out your dispute. They’ll remove errors or prove the info is right. If you win, your score could jump by 50-100 points or more.

Keep copies of everything you send. If you don’t hear back, follow up—don’t let them brush you off.

Pay Outstanding Balances Promptly

Payment history makes up the biggest chunk of your score. Late payments stick around for seven years and can do real damage.

Recent late payments hurt more than old ones. One 30-day late payment could drop your score by 60-110 points, depending on where you started.

Here’s a smart order for tackling payments:

- Knock out past due amounts first

- Always make minimums on every account

- Throw extra at your highest-interest cards

Set up automatic payments to avoid missing due dates. Most banks let you set autopay for at least the minimum, and this helps build credit fast because it keeps your payment history clean.

If you’re struggling, call your lenders before you miss a payment. Many offer payment plans or hardship help.

Lower Your Credit Utilization Rate

Credit utilization counts for 30% of your score. It’s just a fancy way to say: how much of your available credit are you using?

Keep it under 10% for best results. Go above 30% and your score will likely take a hit. If you’ve got $10,000 in total limits, staying under $1,000 is ideal.

Quick ways to lower utilization:

- Pay down balances

- Make more than one payment each month

- Ask for higher credit limits

- Keep old cards open to boost available credit

Lowering utilization can help your score within a month. Card companies report your balance on the statement closing date, not the due date, so timing matters.

Try to pay your balances before the statement closes to show a lower number on your report. It’s a small trick, but it works.

Building Healthy Credit Habits

Good credit habits are the real foundation for a strong score. The big three? Make payments on time (set it and forget it), keep old accounts open, and mix up your types of credit.

Set Up Automatic Payments

Automatic payments can save you from the pain of missed due dates. Since payment history is 35% of your score, you want this locked down.

Banks and card companies let you set up autopay for free. You can pick the minimum payment, the full balance, or a fixed amount each month.

Why automatic payments matter:

- No more missed due dates

- Skip late fees (which can be $25 to $40—yikes)

- Avoid penalty rates up to 29.99%

- Build a rock-solid payment record

Setting up autopay takes just a few minutes online or in your bank’s app. Still, check your statements monthly for mistakes or weird charges.

Worried about overdrafts? Set autopay for just the minimum and pay the rest manually when you can. It’s not perfect, but it’s safer if your balance is tight.

Keep Old Accounts Open

Closing old cards can ding your score in two ways. You lose available credit and your average account age shrinks.

If you have $1,000 of debt and $10,000 in total credit, your utilization is 10%. Close a card with a $5,000 limit and suddenly you’re at 20%.

Length of credit history matters:

- Oldest account age (15% of score)

- Average age of all accounts

- How recently you’ve used your accounts

Closed accounts stay on your report for up to 10 years, but keeping them open is usually better. Make a small purchase every few months to keep cards active and avoid them being closed for inactivity.

If a card charges an annual fee and you’re not getting value, consider asking for a downgrade to a no-fee version. No need to pay for something you don’t use.

Diversify Your Credit Mix

Credit mix makes up 10% of your credit score. Lenders want to see that you can handle different types of credit responsibly.

Main types of credit accounts:

- Revolving credit: Credit cards and lines of credit

- Installment loans: Auto loans, mortgages, student loans

- Open credit: Charge cards that require full payment monthly

Most people start with credit cards. Adding an installment loan later can help your credit mix score.

Auto loans and personal loans are popular as a second type of credit. Student loans count as installment credit too, especially if you’re in school.

Don’t take on debt just to improve your credit mix. This factor matters less than payment history and credit utilization, and the small score bump usually isn’t worth more interest costs.

If you only have one credit card, adding another type of credit can help more. People with multiple accounts already won’t see as much benefit.

Advantages of Boosting Your Credit Score Quickly

A higher credit score opens doors to better financial products. You’ll save money over time, too.

Lower interest rates on loans and credit cards are a huge perk. You’ll also have higher approval odds for big purchases.

Access to Better Interest Rates

Your credit score directly affects the interest rates lenders offer you. If your score is above 740, you’ll usually get the best rates out there.

The difference can be massive. Someone with excellent credit might score a mortgage at 6.5%, while fair credit could mean 8.5%. On a $300,000 loan, that’s around $108,000 in savings over 30 years.

Credit card rates drop with higher scores, too. Excellent credit often means rates between 15-18%, while fair credit can mean 22-25% or higher.

Auto loans work the same way. Good credit could lower your monthly payment by $50-100 compared to poor credit.

Improving your credit scores quickly lets you access these better rates sooner. Why wait years if you don’t have to?

Improved Loan Approval Chances

Higher scores give you better odds for loan approval across the board. Lenders see good credit as proof you pay bills on time and handle debt well.

It’s easier to get a mortgage with a score above 620. Many lenders set minimums, and higher scores mean less paperwork.

Personal loan approvals jump with better credit. Some places only work with borrowers above 650 or 700.

Credit card applications get approved more often with higher scores. The best rewards cards usually require excellent credit.

Landlords check credit scores, too. They prefer tenants with solid payment history.

If you’re starting a business, a strong personal credit score can help you qualify for loans, especially if your business is brand new.

Disadvantages and Risks of Rapid Credit Score Increases

Quick credit score jumps sound great, but they’re not always what they seem. Fast fixes often hide risks and sometimes even scams.

Potential Scams and Quick Fix Myths

Credit repair scams target people who want results overnight. These companies claim they’ll erase negative marks from your credit report instantly—for a fee up front.

Watch out for these red flags:

- Promises to raise scores by 200+ points fast

- Demands for payment before doing anything

- Claims they can delete accurate negative info

- Pressure to sign up right away

Many disadvantages of rapid credit changes start with falling for these schemes. Real credit repair takes patience.

The Federal Trade Commission warns that no company can legally remove accurate info from your reports. You can dispute errors yourself for free with the credit bureaus.

Myth: Paying off all debt instantly boosts your score by 100 points.

Reality: Utilization changes usually show up after 1-2 billing cycles.

Temporary Effects Versus Long-Term Impact

Fast credit score boosts often fade within a few months. These quick wins can make people overconfident when borrowing.

Temporary tactics that backfire:

- Opening several new accounts at once

- Briefly becoming an authorized user

- Making big payments right before applying

Even one late payment can drop your credit score a lot. Quick fixes are fragile.

Building good credit really takes time. Payment history makes up 35% of your score, and you can’t rush that.

People chasing rapid increases sometimes forget the basics. Missing payments after hitting a target score can cause big drops.

Long-term building means:

- Paying on time for at least 6 months

- Cutting debt gradually

- Keeping old accounts open for a longer credit history

Beginner Credit Tools and Resources

If you’re new to credit, you’ve got some great tools to get started. Secured credit cards are the easiest entry point, while credit builder loans help you establish a positive payment history even if you don’t have any credit yet.

Secured Credit Cards

Secured credit cards need a cash deposit, which becomes your credit limit. Most require $200 to $500 up front, and that money sits in a savings account while you use the card.

These cards report to all three credit bureaus, just like regular cards. Make small purchases and pay off the full balance each month. That way, you build payment history without racking up interest charges.

Best practices for secured cards:

- Pick cards with no annual fees

- Look for ones that “graduate” you to unsecured cards

- Keep your balance below 10% of your limit

- Set up autopay to avoid late fees

Many secured cards upgrade you to unsecured after 6-12 months of good payments. You’ll get your deposit back. Some even add rewards after you graduate.

Credit Builder Loans

Credit builder loans flip the usual loan process. The lender puts the loan amount in a savings account, and you pay it off monthly. When you finish, you get the money (plus any interest earned).

Loan amounts usually range from $300 to $1,000, with terms of 6 to 24 months. Payments are typically $25 to $100 a month. Each payment gets reported to the credit bureaus, helping you build history.

Credit builder loan benefits:

- No credit check needed

- Acts as a forced savings plan

- Interest rates are lower than most credit cards

- Builds payment history from the start

Community banks and credit unions usually have the best deals. Some online lenders offer these loans, too. Make sure to compare fees and rates before you sign up.

Authorized User Strategies

If someone adds you as an authorized user to their credit card, their payment history and utilization show up on your report. This can give your score a quick lift, but it depends on the primary cardholder’s habits.

What you’ll need for this to work:

- The main cardholder must pay on time

- The account should have a low balance (under 30%)

- It helps if the account is at least two years old

- The primary cardholder should keep up their good habits

Parents, spouses, and close family are usually the best people to ask. You don’t have to use the card or even hold it—just being listed helps your credit.

Some authorized users see their scores rise in 30-60 days. But if the main cardholder misses payments, it’ll hurt your score too. This approach only works if you trust their financial habits completely.

Monitoring Your Credit Progress

Tracking your credit score helps you spot problems early and celebrate progress. Regular check-ins show what’s working and keep you moving toward your goals.

How to Track Your Credit Score Over Time

Checking your score every month gives you a clear view of your progress. Free services like Credit Karma, Credit Sesame, and Experian update your numbers every week or month.

Most credit card companies offer free credit scores on your monthly statement. Chase, Capital One, and Discover all show FICO scores at no cost.

Free Credit Score Sources:

- Annual Credit Report (once a year from each bureau)

- Credit card statements every month

- Bank apps and websites

- Credit monitoring services

Set up score alerts to catch sudden changes. Most services will email you if your score jumps or drops by a certain amount.

Track your scores from all three bureaus: Experian, Equifax, and TransUnion. They often show different numbers since not all lenders report to every bureau.

Jotting down your scores in a notebook or spreadsheet helps you see trends. You’ll start to notice which actions make the biggest difference.

Best Practices for Ongoing Credit Health

Check your credit reports every four months to spot errors before they damage your score. Request one free report every four months from each bureau, and you’ll have year-round coverage without spending a dime.

Monthly Credit Tasks:

- Check your credit scores

- Review credit card balances

- Pay all bills on time

- Look for suspicious activity

Set calendar reminders so you never miss a payment. Late payments can stick around on your credit report for seven years and really drag your score down.

Try to keep credit card balances under 10% of your limits. Even if you pay off your cards every month, high balances can still hurt your score.

If you’re just starting out, it’s usually better to keep old credit cards open unless they charge annual fees. Older accounts help lengthen your credit history, which makes up 15% of your score.

Dispute errors on your credit report as soon as you spot them. Credit bureaus have 30 days to investigate and remove anything that’s incorrect.

Key Giveaways

Payment history makes up 35% of your credit score. Paying bills on time is your quickest route to improvement—there’s really no shortcut around that.

Credit utilization should stay below 30% of your available limits. Keep those balances low on every card for the best shot at a higher score.

Quick wins include paying down debt and asking for credit limit increases. These moves can bump your score up in as little as 30-60 days, which is honestly pretty motivating.

Authorized user status on someone else’s account can add positive payment history right away. Just make sure their payment record is spotless first.

Credit monitoring lets you track your progress and catch mistakes early. Tons of apps offer free monthly score updates, so take advantage.

Mix up your credit with both revolving accounts and installment loans if you can. Lenders like to see you handle different types of credit.

| Action | Timeline | Impact |

|---|---|---|

| Pay bills on time | 30 days | High |

| Lower credit utilization | 1-2 months | High |

| Become authorized user | 1-2 months | Medium |

| Dispute errors | 30-45 days | Variable |

Don’t make common mistakes like closing old accounts or applying for too much credit at once. These moves can slow your progress or even set you back.

Patience pays off—credit building isn’t instant. Most folks see real changes after 3-6 months of sticking with good habits.

Free resources like Credit Karma and annual credit reports let you keep tabs on your progress without spending a thing.

Next Steps visit Millennial Credit Advisers

Building excellent credit takes time and steady effort. If you follow these proven strategies, you’ll likely see your score improve within a few months.

The two most important things? Pay your bills on time and keep your credit card balances low. Together, they make up 65% of your score, so they’re worth your focus.

Next Actions to Take:

• Check credit reports from all three bureaus monthly

• Set up automatic payments for every bill

• Apply for a secured credit card if you need to build credit

• Keep old accounts open to help your credit history

Millennial Credit Advisers offers tools and resources that help you reduce debt and raise your score. Their platform includes some pretty slick apps to track your progress, which I wish I’d had starting out.

Lots of people find professional guidance helpful at the start of their credit journey. An expert can help you dodge the classic mistakes that slow down your results.

Warning Signs to Watch:

- Credit utilization above 30%

- Late payments showing up on your report

- Too many hard inquiries in a short time

- Closing old credit accounts

Good credit comes from patience and smart habits. If you stick with the basics, you’ll see your score climb, even if it sometimes feels slow.

Credit repair is a marathon, not a sprint. Build habits you can actually keep up, and don’t fall for quick fixes—they almost always backfire.

Take action today by checking your credit report and spotting areas for improvement. Every small step now opens doors to better financial opportunities down the road.

Start Improving Your Credit Score Today

Start today and you could see your credit score move in the right direction within a few weeks. These strategies really do work, but only if you stick with them.

Start with these immediate steps:

• Check all three credit reports for errors

• Pay down your credit card balances below 30% utilization

• Set up automatic payments for every bill so you never miss one

• Think about becoming an authorized user on a family member’s account

Many beginners notice results in 30-60 days when they focus on practical credit improvement tips. Payment history and utilization move the needle more than anything else.

Track your progress monthly with free credit monitoring tools. That way, you’ll actually see which habits make the biggest difference.

Building good credit doesn’t happen overnight, but even small changes today can make a big impact later. Every positive step adds up.

Your journey to excellent credit starts with a single move. Pick one strategy from this list and put it into action this week.

Remember: Consistency matters more than perfection. It’s better to make steady progress than to try for dramatic changes you can’t keep up with.

Credit improvement is a marathon. Start now and stay with it—you’ll thank yourself later.

Credit scores touch everything—renting an apartment, getting a car loan, sometimes even job offers. If you’re young or new to credit, it’s easy to feel stuck because you don’t have much history or maybe made a few rookie mistakes.

Knowing which steps matter most helps you focus your energy and see actual results. Don’t waste time on stuff that barely moves the needle.

Most beginners see progress by zeroing in on two things: payment history and credit utilization. These two make up 65% of your score.

Pay your bills on time and keep your card balances low. It’s basic, but honestly, these changes can give your score a real lift in just a few months.

Understanding Credit Scores

Most lenders use FICO or VantageScore. Both use similar methods to crunch the numbers.

Credit scores shift every month as banks send in new info. One late payment can drop your score by 60 to 110 points.

Opening a new account can knock your score down by 5 to 10 points for a bit. It’s not forever, but it stings.

How Are Credit Scores Calculated?

Your score comes from five main factors. Each one counts for a different chunk of the total.

FICO Score Breakdown:

- Payment history: 35%

- Credit utilization: 30%

- Length of credit history: 15%

- Credit mix: 10%

- New credit inquiries: 10%

Payment history checks if you pay bills on time. Even one late payment (over 30 days) can hurt.

Credit utilization looks at how much of your available credit you’re using. If you keep your balances under 30% of your total limits, you’re in good shape. Under 10% is even better.

Length of credit history just means how long you’ve had accounts open. Older is better.

Why Credit Scores Matter for Beginners

Credit scores decide which financial products you can get and what rates you’ll pay. Good scores save you a lot of money, plain and simple.

Benefits of Higher Credit Scores:

- Lower interest rates on loans

- Better credit card offers

- Easier time renting apartments

- Lower insurance premiums

- Access to some jobs

If you have a 760 score, you might snag a 6% car loan. With a 620, you could pay 12% for the same car. Ouch.

Landlords check credit, too. Many want to see scores above 650 before handing over the keys.

Some jobs—especially those handling money or security—look at your credit report. Bad credit can close doors in banking or government work.

Start building good credit early and you’ll have more options later. It’s a head start that really pays off when it’s time to buy a home or launch a business.

Quick Steps to Increase Your Credit Score Fast

Let’s get to the good stuff. These three steps can make a difference fast, sometimes in just 30-60 days. Focus on removing errors, paying bills on time, and keeping your credit card balances in check.

Check Your Credit Report for Errors

Millions of Americans have credit report mistakes dragging down their scores. You can grab free reports once a year from each big bureau at AnnualCreditReport.com.

Common issues? Wrong account info, payments marked late when you paid on time, or accounts that aren’t even yours. Sometimes other people’s data gets mixed in—super frustrating.

The dispute process goes through each bureau separately. You can file disputes online, by mail, or over the phone. Disputing errors can wipe out negative marks pretty quickly.

The bureaus get 30 days to check out your dispute. They’ll remove errors or prove the info is right. If you win, your score could jump by 50-100 points or more.

Keep copies of everything you send. If you don’t hear back, follow up—don’t let them brush you off.

Pay Outstanding Balances Promptly

Payment history makes up the biggest chunk of your score. Late payments stick around for seven years and can do real damage.

Recent late payments hurt more than old ones. One 30-day late payment could drop your score by 60-110 points, depending on where you started.

Here’s a smart order for tackling payments:

- Knock out past due amounts first

- Always make minimums on every account

- Throw extra at your highest-interest cards

Set up automatic payments to avoid missing due dates. Most banks let you set autopay for at least the minimum, and this helps build credit fast because it keeps your payment history clean.

If you’re struggling, call your lenders before you miss a payment. Many offer payment plans or hardship help.

Lower Your Credit Utilization Rate

Credit utilization counts for 30% of your score. It’s just a fancy way to say: how much of your available credit are you using?

Keep it under 10% for best results. Go above 30% and your score will likely take a hit. If you’ve got $10,000 in total limits, staying under $1,000 is ideal.

Quick ways to lower utilization:

- Pay down balances

- Make more than one payment each month

- Ask for higher credit limits

- Keep old cards open to boost available credit

Lowering utilization can help your score within a month. Card companies report your balance on the statement closing date, not the due date, so timing matters.

Try to pay your balances before the statement closes to show a lower number on your report. It’s a small trick, but it works.

Building Healthy Credit Habits

Good credit habits are the real foundation for a strong score. The big three? Make payments on time (set it and forget it), keep old accounts open, and mix up your types of credit.

Set Up Automatic Payments

Automatic payments can save you from the pain of missed due dates. Since payment history is 35% of your score, you want this locked down.

Banks and card companies let you set up autopay for free. You can pick the minimum payment, the full balance, or a fixed amount each month.

Why automatic payments matter:

- No more missed due dates

- Skip late fees (which can be $25 to $40—yikes)

- Avoid penalty rates up to 29.99%

- Build a rock-solid payment record

Setting up autopay takes just a few minutes online or in your bank’s app. Still, check your statements monthly for mistakes or weird charges.

Worried about overdrafts? Set autopay for just the minimum and pay the rest manually when you can. It’s not perfect, but it’s safer if your balance is tight.

Keep Old Accounts Open

Closing old cards can ding your score in two ways. You lose available credit and your average account age shrinks.

If you have $1,000 of debt and $10,000 in total credit, your utilization is 10%. Close a card with a $5,000 limit and suddenly you’re at 20%.

Length of credit history matters:

- Oldest account age (15% of score)

- Average age of all accounts

- How recently you’ve used your accounts

Closed accounts stay on your report for up to 10 years, but keeping them open is usually better. Make a small purchase every few months to keep cards active and avoid them being closed for inactivity.

If a card charges an annual fee and you’re not getting value, consider asking for a downgrade to a no-fee version. No need to pay for something you don’t use.

Diversify Your Credit Mix

Credit mix makes up 10% of your credit score. Lenders want to see that you can handle different types of credit responsibly.

Main types of credit accounts:

- Revolving credit: Credit cards and lines of credit

- Installment loans: Auto loans, mortgages, student loans

- Open credit: Charge cards that require full payment monthly

Most people start with credit cards. Adding an installment loan later can help your credit mix score.

Auto loans and personal loans are popular as a second type of credit. Student loans count as installment credit too, especially if you’re in school.

Don’t take on debt to improve your credit mix. This factor matters less than payment history and credit utilization, and the small score bump usually isn’t worth the additional interest costs.

If you only have one credit card, adding another type of credit can help more. People with multiple accounts already won’t see as much benefit.

Advantages of Boosting Your Credit Score Quickly

A higher credit score opens doors to better financial products. You’ll save money over time, too.

Lower interest rates on loans and credit cards are a huge perk. You’ll also have higher approval odds for big purchases.

Access to Better Interest Rates

Your credit score directly affects the interest rates lenders offer you. If your score is above 740, you’ll usually get the best rates out there.

The difference can be massive. Someone with excellent credit might score a mortgage at 6.5%, while fair credit could mean 8.5%. On a $300,000 loan, that’s around $108,000 in savings over 30 years.

Credit card rates drop with higher scores, too. Excellent credit often means rates between 15-18%, while fair credit can mean 22-25% or higher.

Auto loans work the same way. Good credit could lower your monthly payment by $50-100 compared to poor credit.

Improving your credit scores quickly lets you access these better rates sooner. Why wait years if you don’t have to?

Improved Loan Approval Chances

Higher scores give you better odds for loan approval across the board. Lenders see good credit as proof you pay bills on time and handle debt well.

It’s easier to get a mortgage with a score above 620. Many lenders set minimums, and higher scores mean less paperwork.

Personal loan approvals jump with better credit. Some places only work with borrowers above 650 or 700.

Credit card applications get approved more often with higher scores. The best rewards cards usually require excellent credit.

Landlords check credit scores, too. They prefer tenants with solid payment history.

If you’re starting a business, a strong personal credit score can help you qualify for loans, especially if your business is brand new.

Disadvantages and Risks of Rapid Credit Score Increases

Quick credit score jumps sound great, but they’re not always what they seem. Fast fixes often hide risks and sometimes even scams.

Potential Scams and Quick Fix Myths

Credit repair scams target people who want results overnight. These companies claim they’ll erase negative marks from your credit report instantly—for a fee up front.

Watch out for these red flags:

- Promises to raise scores by 200+ points fast

- Demands for payment before doing anything

- Claims they can delete accurate negative info

- Pressure to sign up right away

Many disadvantages of rapid credit changes start with falling for these schemes. Real credit repair takes patience.

The Federal Trade Commission warns that no company can legally remove accurate info from your reports. You can dispute errors yourself for free with the credit bureaus.

Myth: Paying off all debt instantly boosts your score by 100 points.

Reality: Utilization changes usually show up after 1-2 billing cycles.

Temporary Effects Versus Long-Term Impact

Fast credit score boosts often fade within a few months. These quick wins can make people overconfident when borrowing.

Temporary tactics that backfire:

- Opening several new accounts at once

- Briefly becoming an authorized user

- Making big payments right before applying

Even one late payment can drop your credit score a lot. Quick fixes are fragile.

Building good credit really takes time. Payment history makes up 35% of your score, and you can’t rush that.

People chasing rapid increases sometimes forget the basics. Missing payments after hitting a target score can cause big drops.

Long-term building means:

- Paying on time for at least 6 months

- Cutting debt gradually

- Keeping old accounts open for a longer credit history

Beginner Credit Tools and Resources

If you’re new to credit, you’ve got some great tools to get started. Secured credit cards are the easiest entry point, while credit builder loans help you establish a positive payment history even if you don’t have any credit yet.

Secured Credit Cards

Secured credit cards need a cash deposit, which becomes your credit limit. Most require $200 to $500 up front, and that money sits in a savings account while you use the card.

These cards report to all three credit bureaus, just like regular cards. Make small purchases and pay off the full balance each month. That way, you build payment history without racking up interest charges.

Best practices for secured cards:

- Pick cards with no annual fees

- Look for ones that “graduate” you to unsecured cards

- Keep your balance below 10% of your limit

- Set up autopay to avoid late fees

Many secured cards upgrade you to unsecured after 6-12 months of good payments. You’ll get your deposit back. Some even add rewards after you graduate.

Credit Builder Loans

Credit builder loans flip the usual loan process. The lender puts the loan amount in a savings account, and you pay it off monthly. When you finish, you get the money (plus any interest earned).

Loan amounts usually range from $300 to $1,000, with terms of 6 to 24 months. Payments are typically $25 to $100 a month. Each payment gets reported to the credit bureaus, helping you build history.

Credit builder loan benefits:

- No credit check needed

- Acts as a forced savings plan

- Interest rates are lower than most credit cards

- Builds payment history from the start

Community banks and credit unions usually have the best deals. Some online lenders offer these loans, too. Make sure to compare fees and rates before you sign up.

Authorized User Strategies

If someone adds you as an authorized user to their credit card, their payment history and utilization show up on your report. This can give your score a quick lift, but it depends on the primary cardholder’s habits.

What you’ll need for this to work:

- The main cardholder must pay on time

- The account should have a low balance (under 30%)

- It helps if the account is at least two years old

- The primary cardholder should keep up their good habits

Parents, spouses, and close family are usually the best people to ask. You don’t have to use the card or even hold it—just being listed helps your credit.

Some authorized users see their scores rise in 30-60 days. But if the main cardholder misses payments, it’ll hurt your score too. This approach only works if you trust their financial habits completely.

Monitoring Your Credit Progress

Tracking your credit score helps you spot problems early and celebrate progress. Regular check-ins show what’s working and keep you moving toward your goals.

How to Track Your Credit Score Over Time

Checking your score every month gives you a clear view of your progress. Free services like Credit Karma, Credit Sesame, and Experian update your numbers every week or month.

Most credit card companies offer free credit scores on your monthly statement. Chase, Capital One, and Discover all show FICO scores at no cost.

Free Credit Score Sources:

- Annual Credit Report (once a year from each bureau)

- Credit card statements every month

- Bank apps and websites

- Credit monitoring services

Set up score alerts to catch sudden changes. Most services will email you if your score jumps or drops by a certain amount.

Track your scores from all three bureaus: Experian, Equifax, and TransUnion. They often show different numbers since not all lenders report to every bureau.

Jotting down your scores in a notebook or spreadsheet helps you see trends. You’ll start to notice which actions make the biggest difference.

Best Practices for Ongoing Credit Health

Check your credit reports every four months to spot errors before they damage your score. Request one free report every four months from each bureau, and you’ll have year-round coverage without spending a dime.

Monthly Credit Tasks:

- Check your credit scores

- Review credit card balances

- Pay all bills on time

- Look for suspicious activity

Set calendar reminders so you never miss a payment. Late payments can stick around on your credit report for seven years and really drag your score down.

Try to keep credit card balances under 10% of your limits. Even if you pay off your cards every month, high balances can still hurt your score.

If you’re just starting out, it’s usually better to keep old credit cards open unless they charge annual fees. Older accounts help lengthen your credit history, which makes up 15% of your score.

Dispute errors on your credit report as soon as you spot them. Credit bureaus have 30 days to investigate and remove anything that’s incorrect.

Key Giveaways

Payment history makes up 35% of your credit score. Paying bills on time is your quickest route to improvement—there’s really no shortcut around that.

Credit utilization should stay below 30% of your available limits. Keep those balances low on every card for the best shot at a higher score.

Quick wins include paying down debt and asking for credit limit increases. These moves can bump your score up in as little as 30-60 days, which is honestly pretty motivating.

Authorized user status on someone else’s account can add positive payment history right away. Just make sure their payment record is spotless first.

Credit monitoring lets you track your progress and catch mistakes early. Tons of apps offer free monthly score updates, so take advantage.

Mix up your credit with both revolving accounts and installment loans if you can. Lenders like to see you handle different types of credit.

| Action | Timeline | Impact |

|---|---|---|

| Pay bills on time | 30 days | High |

| Lower credit utilization | 1-2 months | High |

| Become authorized user | 1-2 months | Medium |

| Dispute errors | 30-45 days | Variable |

Don’t make common mistakes like closing old accounts or applying for too much credit at once. These moves can slow your progress or even set you back.

Patience pays off—credit building isn’t instant. Most folks see real changes after 3-6 months of sticking with good habits.

Free resources like Credit Karma and annual credit reports let you keep tabs on your progress without spending a thing.

Visit Millennial Credit Advisers

Building excellent credit takes time and steady effort. If you follow these proven strategies, you’ll likely see your score improve within a few months.

The two most important things? Pay your bills on time and keep your credit card balances low. Together, they make up 65% of your score, so they’re worth your focus.

Next Actions to Take:

• Check credit reports from all three bureaus monthly

• Set up automatic payments for every bill

• Apply for a secured credit card if you need to build credit

• Keep old accounts open to help your credit history

Millennial Credit Advisers offers tools and resources that help you reduce debt and raise your score. Their platform includes some pretty slick apps to track your progress, which I wish I’d had starting out.

Lots of people find professional guidance helpful at the start of their credit journey. An expert can help you dodge the classic mistakes that slow down your results.

Warning Signs to Watch:

- Credit utilization above 30%

- Late payments showing up on your report

- Too many hard inquiries in a short time

- Closing old credit accounts

Good credit comes from patience and smart habits. If you stick with the basics, you’ll see your score climb, even if it sometimes feels slow.

Credit repair is a marathon, not a sprint. Build habits you can actually keep up, and don’t fall for quick fixes—they almost always backfire.

Take action today by checking your credit report and spotting areas for improvement. Every small step now opens doors to better financial opportunities down the road.

Start Improving Your Credit Score Today

Start today and you could see your credit score move in the right direction within a few weeks. These strategies really do work, but only if you stick with them.

Start with these immediate steps:

• Check all three credit reports for errors

• Pay down your credit card balances below 30% utilization

• Set up automatic payments for every bill so you never miss one

• Think about becoming an authorized user on a family member’s account

Many beginners notice results in 30-60 days when they focus on practical credit improvement tips. Payment history and utilization move the needle more than anything else.

Track your progress monthly with free credit monitoring tools. That way, you’ll actually see which habits make the biggest difference.

Building good credit doesn’t happen overnight, but even small changes today can make a big impact later. Every positive step adds up.

Your journey to excellent credit starts with a single move. Pick one strategy from this list and put it into action this week.

Remember: Consistency matters more than perfection. It’s better to make steady progress than to try for dramatic changes you can’t keep up with.

Credit improvement is a marathon. Start now and stay with it—you’ll thank yourself later.

Frequently Asked Questions

New credit users usually have a lot of questions about timelines and what actually works. Here are some answers to the most common concerns about building strong credit foundations and boosting scores quickly.

What are effective strategies for boosting your credit score quickly as a beginner?

If you’re new to credit, focus on payment history and utilization. Pay every bill on time—seriously, that’s non-negotiable.

Keep your credit card balances under 30% of your limits. Lenders want to see that you’re using credit responsibly, not maxing out cards.

Getting added as an authorized user on someone else’s account can boost your score pretty quickly. Just make sure their payment habits are rock-solid.

Paying down debt lowers your utilization ratio, sometimes within a single billing cycle. That can bump your score up in 30-60 days, which feels pretty good.

Are there any actions one can take to potentially increase their credit score by 100 points within a month?

Hitting a 100-point jump in just a month is rare, but it happens if you have a lot of room to improve. Folks with very low scores can see bigger leaps.

Pay off high credit card balances and you’ll often see a quick score spike. Utilization updates as soon as your next statement posts.

Dispute any errors on your credit report right away. Getting rid of inaccurate late payments or collections can really help.

Ask to be added as an authorized user on an account with a perfect history. The impact depends on the card’s limits and payment record.

What steps are needed to achieve a credit score of 800 or higher?

If you want to hit 800, you’ll need years of on-time payments. No late payments—ever—and a squeaky-clean record.

Keep your utilization below 10% on every account. Most people with 800+ scores use less than 5% of their available credit.

Have a mix of credit cards, auto loans, or mortgages. Lenders like to see that you can manage different types of accounts.

Keep your oldest accounts open. A long credit history makes a big difference once you’re aiming for the top tier.

How long does it typically take to see a credit score improve by 20 points?

Most people can see a 20-point gain in 1-3 months if they’re consistent. Payment history and utilization drive most of the change.

If your credit is poor, you might see a jump faster. If it’s already good, progress can take a bit longer.

Paying down balances is the fastest way to see a 20-point bump. Credit utilization updates every month when your statement closes.

Building new positive payment history takes a few months to show up. Three months of perfect payments usually brings noticeable improvement.

What methods can lead to an instant increase in credit score?

There’s really no magic bullet, but some actions help fast. Pay down your credit card balances before the statement date for a quick boost.

Dispute obvious errors on your credit report—getting negative marks removed can help in under a month. Credit bureaus have to check within 30 days.

Ask for a credit limit increase but don’t use the extra credit. That drops your utilization instantly if your balances stay the same.

Get added as an authorized user on a good account. Sometimes you’ll see a bump within weeks, depending on when the account updates with the bureaus.

How can beginners establish and build up their credit score effectively?

If you’re just starting out, try a secured credit card or maybe a student credit card. These usually don’t ask for much credit history.

Buy something small, pay it off in full every month, and you’ll start building a positive track record. Lenders notice when you use credit responsibly.

Honestly, setting up automatic payments is a lifesaver—it keeps you from missing due dates. Payment history counts for about 35% of your score, so it’s a big deal.

Check your credit reports now and then. You can grab free ones at annualcreditreport.com and see what all three bureaus have on file.

Disclaimer: Millennial Credit Advisers is not a licensed credit service provider or financial advisor. We do not offer credit repair, debt management, or legal services. Educate yourself on saving, reducing debt, and managing credit for economic improvement. Understand credit reports, scores, and financial products. Consult a financial advisor for personalized guidance. Track your progress for an improved credit journey.

Written content – “Please view our complete AI Use Disclosure.”

We enhance our products and advertising by using Microsoft Clarity to understand how you interact with our website. Using our site, you agree that we and Microsoft can collect and utilize this data. Our privacy policy provides further details.